The order to cash process is the backbone of your revenue cycle. It covers everything from the moment a customer places an order to the moment cash lands in your account. When it runs cleanly, DSO stays low and cash flow is predictable. When it doesn’t, delays compound quickly: follow-ups slip, disputes stall payments, and your finance team spends its time firefighting instead of leading.

So what is order to cash and why does it matter? Understanding the structure is one thing. Understanding where it breaks, and how to fix it, is what improves cash flow.

In this guide, we’ll give a step-by-step breakdown of each O2C stage. We’ll also cover the benefits of an optimized O2C process along with common challenges you may come across, before exploring the role of technology and AI in successful O2C execution.

What Is Order to Cash (O2C)?

Order to cash (O2C), sometimes abbreviated as OTC, is the end-to-end process that begins when a customer places an order and ends when payment is received and recorded. It cuts across sales operations, logistics, finance, and customer service, making it one of the most cross-functional processes in any B2B business.

Why does it matter? Because every delay, error, or bottleneck in the O2C cycle has a direct impact on cash flow.

- A slow invoicing process pushes out collection timelines.

- A credit management failure creates bad debt exposure.

- Poor cash application creates reconciliation backlogs.

Optimizing O2C isn’t an accounting exercise. It’s a strategic priority.

Quote to Cash (QTC) vs. Order to Cash: What’s the Difference?

- Quote to Cash (QTC): Starts at the quoting stage, covering configure-price-quote (CPQ), contract creation, contract lifecycle management, and pre-sales activities.

- Order to Cash (O2C): Starts when a customer order is confirmed. It runs inside the broader QTC framework.

- When QTC matters most: Businesses with complex pricing, subscription billing, or contract-driven revenue need QTC management to control how revenue is recognized and how deal changes flow through the system.

Procure-to-Pay (P2P) vs. Order to Cash: What’s the Difference?

- Procure to Pay (P2P): The buyer-side process. Covers requisitioning, purchase order creation, goods receipt, invoice matching, and accounts payable.

- Order to Cash (O2C): The seller-side process. Covers receiving customer orders and collecting payment for goods or services sold.

- The key distinction: P2P is an accounts payable function. O2C is an accounts receivable function. Data flows in opposite directions and the stakeholders have different priorities.

The Order to Cash Process: A Step-by-Step Guide

The O2C cycle typically runs across nine core stages. Each one is a potential point of failure if handled manually or in isolation.

1. Order Management

- What it is: Capturing, validating, and routing a customer order into your systems accurately.

- What goes wrong: Manual order entry introduces errors that cascade downstream into fulfillment and billing.

- How to address it: Automated validation at the point of entry catches discrepancies before they propagate.

2. Credit Management

- What it is: Assessing customer creditworthiness and setting appropriate credit terms before fulfillment begins.

- What goes wrong: Static credit checks run at onboarding miss changes in customer financial health.

- How to address it: Dynamic credit scoring using live payment data and external signals gives a current, accurate picture of exposure.

3. Order Fulfillment

- What it is: Picking, packing, and preparing goods or services for delivery.

- What goes wrong: An invoice for a partially fulfilled order creates disputes before the billing cycle has even started.

- How to address it: Accurate fulfillment confirmation should trigger invoice generation automatically, removing manual handoff risk.

4. Shipping and Delivery

- What it is: Physical or digital delivery of the product or service, generating the shipping documentation that underpins the invoice.

- What goes wrong: In international O2C, customs requirements, multi-currency considerations, and documentation gaps all introduce delays.

- How to address it: Electronic Data Interchange (EDI) systems standardize documentation transmission between trading partners.

5. Invoicing

- What it is: Generating and sending an accurate invoice as soon as delivery is confirmed.

- What goes wrong: Invoice errors, wrong PO references, and missing contract terms are among the top causes of delayed payment.

- How to address it: Automated invoicing and e-invoicing workflows reduce error rates and accelerate the payment cycle.

6. Accounts Receivable Management

- What it is: Tracking payment due dates, monitoring aging buckets, and prioritizing follow-up across outstanding invoices.

- What goes wrong: When upstream stages are handled poorly, AR management becomes a daily scramble rather than a structured workflow.

- How to address it: A clean upstream process, connected systems, and automated prioritization keep AR predictable and manageable.

7. Payment Collection

- What it is: Active outreach on outstanding invoices, handling payment commitments, and offering frictionless payment options.

- What goes wrong: Inconsistent follow-up lets overdue invoices age without challenge.

- How to address it: A structured, automated outreach sequence ensures timely, context-aware communication across every account.

8. Cash Application

- What it is: Matching incoming payments to the correct invoices and posting them to the ledger.

- What goes wrong: Partial payments, combined remittances, and vague references make manual matching slow and error-prone.

- How to address it: Automated matching with intelligent exception handling clears backlogs and keeps the ledger current.

9. Reporting and Data Management

- What it is: Measuring how well the O2C cycle performed using key metrics.

- Days Sales Outstanding (DSO): The average number of days to collect payment after a credit sale.

- Cash Conversion Cycle (CCC): How long it takes to convert inventory into revenue.

- Collection Effectiveness Index (CEI): How efficiently the team collects its outstanding invoices.

Benefits of an Optimized Order to Cash Process

When the O2C cycle runs efficiently, the impact shows up across multiple dimensions of business performance.

- Improved cash flow: Faster invoicing, consistent follow-up, and frictionless payment options reduce DSO and bring cash in sooner.

- Reduced revenue leakage: Automated validation and accurate invoicing minimize disputes, billing errors, and write-offs.

- Lower operating costs: Automating manual steps frees AR teams to focus on judgment-intensive work rather than data entry.

- Increased customer satisfaction: Accurate invoices, clear payment terms, and smooth dispute resolution improve customer experience and strengthen commercial relationships.

- Compliance and audit readiness: Structured processes and accurate records make audits less painful and regulatory compliance easier to demonstrate.

Common Challenges in Order to Cash (and How to Address Them)

Most O2C problems aren’t caused by individual failures. They’re caused by fragmented processes, disconnected systems, and manual handoffs that introduce errors at every stage.

- Order entry errors: Automated validation at the point of entry prevents downstream billing and fulfillment problems.

- Credit risk blind spots: Real-time credit scoring using live payment data gives finance teams a current, accurate picture of exposure.

- Billing mistakes: Standardizing and automating the invoicing process, including e-invoicing where possible, reduces error rates significantly.

- Slow payment collection: A structured, automated outreach sequence with multiple payment options keeps overdue accounts moving.

- Cash application backlogs: Automated matching with intelligent exception handling clears manual reconciliation work.

- System integration gaps: Real-time integration across ERP, CRM, payment processors, and AR platforms creates the single view of truth O2C requires.

- Dispute management: Clear ownership, escalation paths, and resolution tracking prevent disputes from stalling collections.

Technology and Automation in Order to Cash

Manual O2C processes don’t scale. As transaction volumes grow, errors and delays grow with them.

Technology addresses this, but only when it moves beyond record-keeping and into execution. The right platform will remove manual steps, connect fragmented systems, and surface the intelligence finance teams need to act faster.

Systems of record create visibility. They centralize data, but they don’t move work forward:

- ERP systems: NetSuite, SAP, and Microsoft Dynamics provide the financial backbone, holding order data, billing records, and receivables in one place.

- CRM systems: Customer relationship management platforms give AR teams the account history, contract terms, and contact details they need to communicate effectively.

Execution is what turns that data into outcomes. This is where modern O2C platforms differ.

- AI-driven execution: AI-forward platforms automate collections workflows, apply payments, monitor credit risk in real time, and surface at-risk accounts before they become bad debt.

- E-invoicing: Electronic invoicing ensures invoices are delivered directly into customer systems at the right moment in the process, reducing delays and keeping the billing cycle moving without manual intervention.

- Data analytics: Real-time reporting on DSO, CEI, and aging gives finance leaders clear performance visibility, so they can adjust strategy while execution continues in the background.

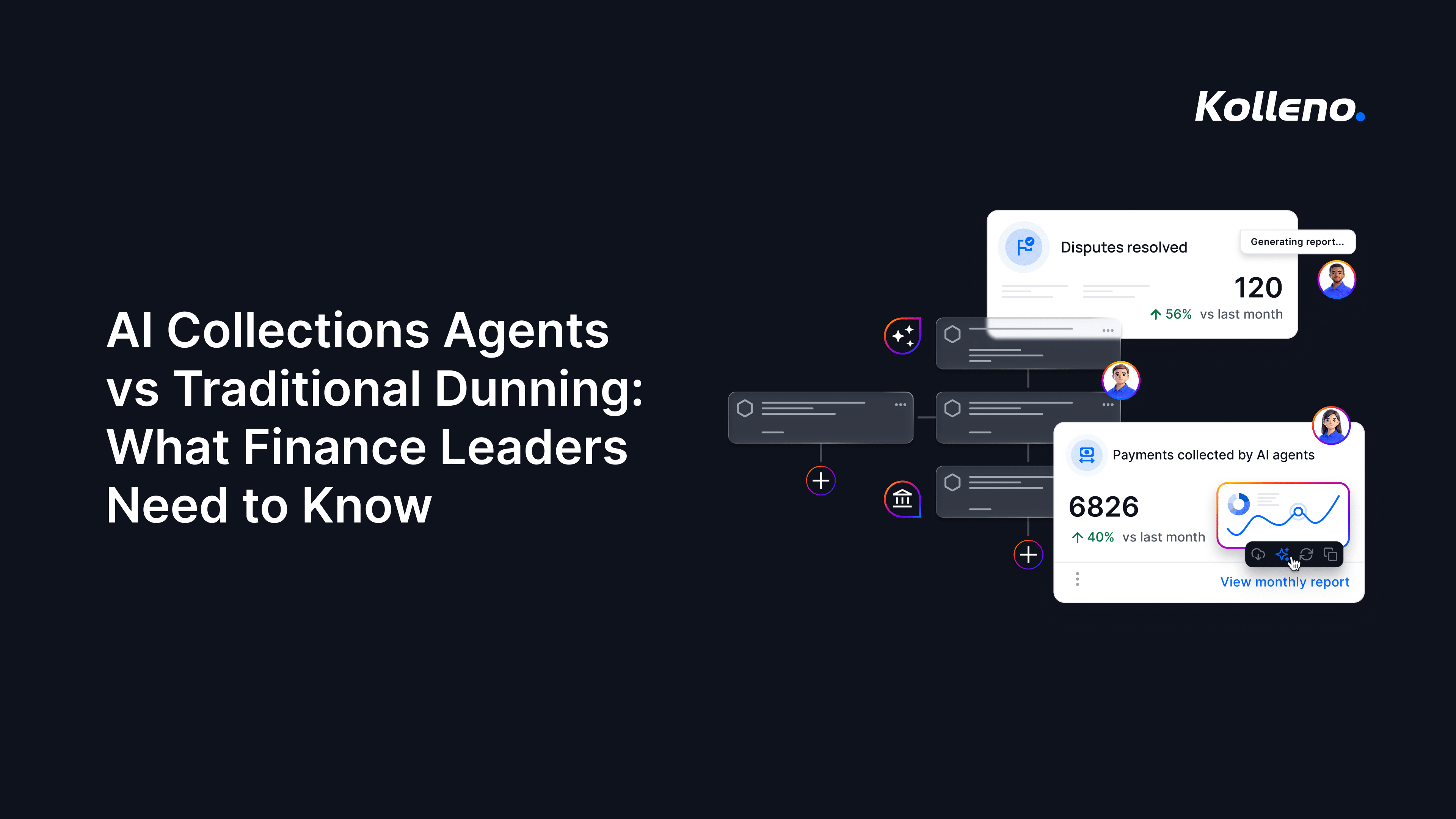

How Kolleno Supports the Order to Cash Cycle

Kolleno is built specifically around the order to cash process. Its Multi-Agent AI Workforce acts as an operational extension of the finance team, handling collections execution, payment processing, cash application, credit risk monitoring, dispute management, and forecasting in a single platform.

Finance teams orchestrate the process by setting policy and objectives. Kolleno’s Maestro AI routes work to the right task-specific AI Agents, sequences their actions, and keeps execution consistent across every account. Your people stay in control. The agents handle the volume.

- ERP integrations: NetSuite, Salesforce, HubSpot, Xero, QuickBooks, Microsoft Dynamics 365, Sage Intacct, Oracle Fusion, and SAP.

- Full O2C coverage: Collections, payments, cash application, credit risk, disputes, and forecasting in one connected platform.

- Human in the loop: Finance teams set the strategy. AI Agents execute it. You retain full visibility and control.

Final Thoughts

The order to cash process connects every revenue-generating activity in your business to actual collected cash. Getting it right means fewer disputes, lower DSO, better cash flow visibility, and a finance team that spends its time on strategy rather than administrative backlog. If you want to see what an AI-powered O2C platform looks like in practice, book a demo of Kolleno.

- What Is Order to Cash (O2C)?

- Quote to Cash (QTC) vs. Order to Cash: What’s the Difference?

- Procure-to-Pay (P2P) vs. Order to Cash: What’s the Difference?

- The Order to Cash Process: A Step-by-Step Guide

- Benefits of an Optimized Order to Cash Process

- Common Challenges in Order to Cash (and How to Address Them)

- Technology and Automation in Order to Cash

- How Kolleno Supports the Order to Cash Cycle

- Final Thoughts