In B2B transactions, companies often extend credit to clients, allowing them to pay for goods or services later. These unpaid amounts are recorded as accounts receivable. Day sales outstanding (DSO) measures how long it takes clients to pay their debts. Quicker payment conversion allows companies to reinvest funds sooner, making DSO a crucial operational metric to track.

This blog will provide a comprehensive guide to DSO, allowing you to fully understand its implications for the business.

In this blog, we will cover:

- Defining the Days Sales Outstanding Ratio

- Understanding the Days Sales Outstanding Ratio

- Interpreting the Days Sales Outstanding Value and its Implication for Businesses

- The Benefits of Tracking Days Sales Outstanding Regularly and Its Applications

- What are the Limitations of the Days Sales Outstanding’s Relevance?

- How Could Companies Lower Their Days Sales Outstanding Figures?

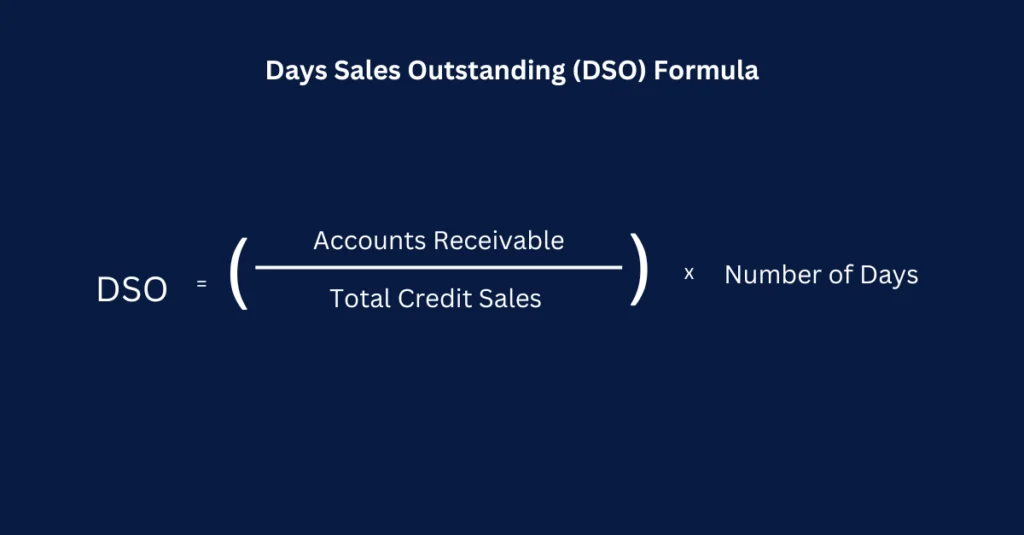

Defining the Days Sales Outstanding Ratio (DSO calculation)

DSO is a key performance indicator for accounts receivables, typically evaluated monthly or quarterly.

The days sales outstanding (DSO) ratio measures the average number of days a firm usually takes to collect cash after it has closed a sale transaction. Here’s the days sales outstanding formula (DSO formula) to calculate days sales outstanding:

Understanding the Days Sales Outstanding Ratio

Collecting outstanding accounts receivables quickly is crucial for maintaining healthy cash flow. While companies can generally expect payment, delays result in lost value due to the time value of money concept.

The definition of “quick” collection varies by industry:

- Extended credit periods are common in finance

- Energy and agriculture sectors prioritize secured debt settlements

- Smaller firms typically depend more on stable cash flow than large corporations with diverse revenue streams

Interpreting the Days Sales Outstanding Value and its Implication for Businesses

DSO provides valuable insights into a company’s cash flow health, considering only credit sales to maintain accuracy. A high DSO may indicate several issues, including long wait times for customer payments, clients with poor credit ratings, extended credit terms to boost sales, declining customer satisfaction, or cash flow problems.

Conversely, a low DSO suggests prompt payment collection, enabling faster business growth. It’s crucial to monitor DSO trends over time to identify patterns in cash flow performance and account for seasonal fluctuations in some businesses. While volatile DSO may be concerning, consistent seasonal changes might be normal for certain industries.

Importantly, DSO interpretation depends on company size and context. For instance, a 45-day DSO is generally considered good, but it may still be worrying for small businesses with tight cash flow. Therefore, it’s essential to always consider the specific context when analyzing DSO, as its implications can vary significantly based on a company’s unique circumstances.

The Benefits of Tracking Days Sales Outstanding Regularly and Its Applications

Regular tracking of Days Sales Outstanding (DSO) offers businesses valuable insights into various aspects of their operations. It helps assess customer payment speed, company liquidity, sales performance, customer satisfaction, and the effectiveness of sales and customer service teams.

By tracking DSO, management can make informed adjustments to business practices. These might include improving payment collection strategies, enhancing customer service training, refining sales policies on payment terms and client selection, identifying consistently late-paying clients, and developing comprehensive credit check policies.

What are the Limitations of the Days Sales Outstanding’s Relevance?

Although the Days Sales Outstanding (DSO) ratio has practical applications in helping analysts determine a company’s efficiency at managing their credit sales conversion to cash, there are several limitations associated with DSO that need to be considered for a comprehensive analysis.

Industry and Company Size Comparisons

DSO comparisons are most meaningful between companies in the same industry with similar revenue and business models. Comparing across different sectors or company sizes can lead to misleading results, as firms often have different DSO benchmarks based on their business nature. For example, a small tech startup might have very different payment terms and cash conversion cycles compared to a large, established manufacturing company.

Moreover, industry norms can significantly impact DSO. Some sectors, like construction or government contracting, typically have longer payment cycles, resulting in higher DSO values that might be considered normal for that industry but problematic in others.

Credit Sales Proportion

The DSO metric has limited applicability when comparing companies with significantly different proportions of credit sales. Businesses with few credit sales lack sufficient data for meaningful DSO analysis, making comparisons with companies that primarily use credit sales less insightful.

For instance, a retail company that mostly deals in cash transactions will have a very different DSO profile compared to a B2B software company that primarily operates on credit terms. In such cases, DSO might not provide an accurate representation of the company’s financial health or operational efficiency.

Fluctuations in Sales Performance

DSO isn’t a perfect measure of the average accounts receivable efficiency, as it can be skewed by fluctuating sales performances or increased cash sales volume. A sudden spike in sales near the end of a reporting period, for example, could artificially inflate the DSO, even if the company’s collection practices haven’t changed.

Seasonal businesses may also see significant variations in their DSO throughout the year, which could lead to misinterpretation if not properly contextualized. For instance, a retailer might see a spike in DSO following the holiday season, which could be misinterpreted as a decline in efficiency if not viewed in the context of their annual sales cycle.

Need for Complementary Metrics

To gain a more comprehensive view of a company’s credit collection capabilities, analysts should consider DSO alongside other metrics. One such metric is the Delinquent Days Sales Outstanding (DDSO), which focuses specifically on overdue receivables.

Other relevant metrics might include:

- Average Collection Period (ACP)

- Accounts Receivable Turnover Ratio

- Collection Effectiveness Index (CEI)

- Bad Debt to Sales Ratio

DSO should be used as part of a broader analysis of working capital metrics rather than as a standalone indicator. This holistic approach provides a more accurate picture of a company’s overall financial health and operational efficiency.

How Could Companies Lower Their Days Sales Outstanding Figures?

Companies can employ various strategies to lower their DSO values, including:

Incentivize Prompt Payments

Offer attractive rewards for clients who pay early to accelerate payment procedures. These incentives could include discounts on future purchases, priority service, or exclusive access to new products. Conversely, implement a structured penalty system for consistently late payments, such as interest charges or reduced credit limits. Ensure all invoices clearly state the terms and conditions regarding payment timing, including both the incentives for early payment and the consequences of late payment. This transparent approach encourages clients to prioritize timely payments and helps maintain a better cash flow for your business.

Expand Payment Options

Increase the range of acceptable payment methods to settle accounts receivables faster. This could include bank transfers, credit card transactions, mobile payments, and even cryptocurrency for tech-savvy clients. Offering a variety of online payment options typically enables quicker payments compared to traditional offline methods. Additionally, consider implementing a customer portal where clients can view their account status, outstanding invoices, and make payments easily. By providing flexible and convenient payment options, you reduce barriers to payment and increase the likelihood of prompt settlements.

Maintain Client Payment Records

For subscription-based businesses, implementing an auto-charging system can effectively manage DSO. Securely store client credit card details for automatic monthly charges, ensuring compliance with data protection regulations. Clearly inform customers about this policy during the onboarding process and provide options for updating payment information. Set up a system to notify customers of each payment processed, including the amount charged and the service period covered. This proactive communication helps prevent disputes and maintains transparency in your billing process, contributing to better client relationships and more predictable cash flow.

Terminate Relationships with Problematic Clients

While customer retention is generally important for business growth, it’s crucial to evaluate the impact of consistently late-paying clients on your cash flow and operations. Conduct a thorough cost-benefit analysis for maintaining relationships with these clients, considering factors such as payment history, profitability, potential for future growth, and the resources required to manage their accounts. If the costs and risks outweigh the benefits, consider implementing a gradual exit strategy. This might involve raising prices, reducing credit limits, or ultimately terminating the business relationship. Be sure to communicate clearly and professionally throughout this process, and have a plan in place to mitigate any potential negative impacts on your business.

Implement Online Invoicing Software

Invest in robust online invoicing software to streamline and automate your payment collection process. This technology can significantly reduce manual tasks, minimize errors, and free up your team’s time for more strategic activities. Look for software that enables prompt invoicing immediately after service delivery or product shipment, provides real-time monitoring of payment status, and allows you to set up customized, automated payment reminders. Advanced systems may also offer features like customizable invoice templates, integration with your accounting software, and detailed reporting capabilities. By leveraging these tools, you can improve the efficiency of your accounts receivable process, reduce DSO, and gain valuable insights into your cash flow patterns.

Consider Kolleno’s AI-powered Accounts Receiavble Platform

Kolleno offers a comprehensive solution for businesses seeking to lower DSO values. Its accounts receivable software automates manual procedures, delivers well-crafted dinning emails promptly, sets appropriate credit terms, and manages payment collections systematically.

Using Kolleno improves liquidity and shorten the credit-to-cash cycle, fostering long-term business development opportunities.

Learn how DNA Payments have used Kolleno and NetSuite’s Integration to reduce their overdue balances by 34% in just the first 3 months of using Kolleno.

Concluding Thoughts

The days sales outstanding (DSO) ratio is an essential metric that B2B-centric companies need to track in order to assess their business’s financial health. The lower the DSO value, the less time it takes a business to convert their credit sales into capital, which suggests a healthier cash flow. Conversely, the higher the DSO ratio, the long it takes for clients to settle their outstanding accounts receivables.

To help achieve lower DSO, finance professionals should consider Kolleno, a smart AR management platform. Kolleno offers an all-in-one accounts receivable software solution. Its AI-powered credit control system, combined with high-quality customer support, provides customized services to help firms manage their DSO ratios in a much more effective manner.

Frequently Asked Questions (FAQs)

What are Days Sales Outstanding (DSO)?

Days sales outstanding (DSO) can be defined as the mean number of days a company takes to have its clients repay their debts for a previous sales transaction. In other words, DSO represents how long a firm takes to collect its outstanding accounts receivables.

How is the Days Sales Outstanding Value Calculated?

The DSO ratio can be calculated by dividing the total amount of accounts receivable a company has within a specific period of time by the total dollar value of its total credit sales during the same timeframe. Following that, this figure should be multiplied by the number of days in the measured duration.

What Would Be Considered a Good Days Sales Outstanding Ratio?

A healthy or concerning DSO ratio would largely depend on the nature of the business and the industry verticals in which the firm is operating. Having mentioned that, maintaining a DSO below 45 days would often be considered the best practice for the majority of companies, as it indicates that the company has a reasonably healthy operational cash flow and thereby has enough money which it can readily reinvest into its business.

- Defining the Days Sales Outstanding Ratio (DSO calculation)

- Understanding the Days Sales Outstanding Ratio

- Interpreting the Days Sales Outstanding Value and its Implication for Businesses

- The Benefits of Tracking Days Sales Outstanding Regularly and Its Applications

- What are the Limitations of the Days Sales Outstanding’s Relevance?

- How Could Companies Lower Their Days Sales Outstanding Figures?

- Concluding Thoughts

- Frequently Asked Questions (FAQs)