The promise of new markets can be intoxicating: access to millions of potential customers, diversification of revenue streams, and the prestige of becoming a truly global brand. But as any CFO or finance leader will tell you, international expansion also carries hidden costs, and if you are not prepared, they can erode profitability, suck up resources, and introduce compliance headaches you never saw coming.

In our recent webinar—hosted by Visa, Tipalti and Kolleno, three industry leaders unpacked the real complexities of cross-border growth and shared strategies to manage them effectively.

In this blog, we’ll explore the key insights discussed.

Four Pillars of International Growth

Successful expansion is not just about opening a new office or translating your website. It requires alignment across four key areas:

- Human Resources

- Relocation vs. local hires

- Recruitment & onboarding processes

- Employer of Record (EoR) vs. updating tech to support global teams

- Compliance with local benefits and labor laws

- Marketing

- Refining your ideal customer profile (ICP) for each market

- Building brand awareness in new regions

- Cultural and language localization

- Finance

- Managing foreign exchange (FX) and banking relationships

- Tax registrations, filings, and reporting nuances

- Payment consolidation vs. fragmentation

- Tech Stack

- Integrating or adapting your ERP system

- Streamlining payments (AR & AP), expenses, T&E, and payroll

- Ensuring tax compliance through automated tools

Neglect one pillar, and your growth engine can break down—delays in payroll, siloed data, tax penalties, or a lack of visibility that makes strategic decision-making impossible.

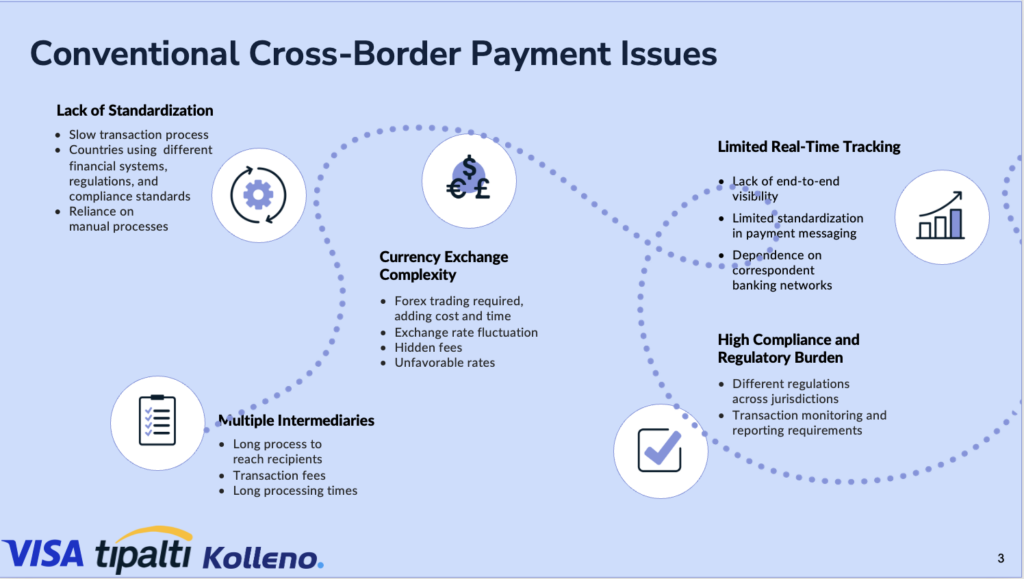

The Hidden Costs of Cross-Border Payments

When it comes to moving money across borders, what seems like a straightforward transaction often masks layers of complexity and expense that can quietly erode your margins and frustrate your stakeholders. Let’s unpack each of the five core frictions to understand how and why they arise, and what they really cost your business.

1. Lengthy Processes & Multiple Intermediaries

A single international payment can pass through several correspondent banks before reaching its destination. Each handoff requires reconciliation, formatting translation, and sometimes manual intervention.

- Multiple Hops: A payment from your UK office to a supplier in Brazil might first route through a London correspondent, then a New York intermediary, before landing in São Paulo. Each step adds 1–2 business days of delay.

- Operational Overhead: Every intermediary relationship demands account setup, compliance checks, and ongoing maintenance, tying up treasury staff in routine follow-ups.

- Real-Cost Example: If your average payment value is £50,000 and it takes four extra days to settle, you’re effectively extending your working capital cycle by 4× your daily cost of capital. For a company with a 10% annual funding cost, that’s roughly £50 per £50,000 each day, adding up fast.

2. Transaction Fees & Unfavorable Rates

Fees levied by each bank in the chain quickly compound, and the FX rate you see publicly is rarely the one you get.

- Layered Fees: Correspondent banks typically charge a fixed fee (e.g., $15–$30) plus a percentage of the transaction. If three banks are involved, you might pay $75–$120 in fees on a single transfer.

- Hidden FX Markups: Major banks often embed a 1–3% margin on top of the mid-market exchange rate. On a €1 million invoice, that hidden spread alone can be €10,000–€30,000.

- Example Calculation: A U.S. company paying CAD 200,000 incurs:

- $25 fixed fee × 3 intermediaries = $75

- 2% FX markup on CAD–USD conversion ≈ $4,000

- Total cost: $4,075 or 2.04% of the transaction value

3. Regulatory & Compliance Burdens

Different jurisdictions impose their own Know-Your-Customer (KYC), Anti-Money Laundering (AML), and sanctions checks, often with no standardized approach.

- Divergent KYC Standards: While the EU may require a corporate registry check plus beneficial-owner verification, a non-OECD country might insist on additional notarized documents, each requiring translation and apostille.

- Manual Reviews Inflate Headcount: Every new country or currency introduces fresh documentation requirements. Mid-sized businesses can find themselves dedicating 1–2 full-time employees just to keep up with compliance forms and periodic renewals.

- Sanctions Screening: A single sanctions list update could trigger thousands of payment holds until names are manually verified, leading to released payments only after days of back-and-forth.

4. Lack of End-to-End Visibility

Once funds leave your Enterprise Resource Planning (ERP) system, they often enter a black hole.

- No Real-Time Status: With traditional banking rails, you might only see “in progress” until the beneficiary bank posts the credit, sometimes days later.

- Disparate Messaging Formats: SWIFT MT103 messages vary by bank; reconciling references and remittance details across different formats can take hours per payment.

- Poor Exception Handling: If a payment bounces or gets rejected, alerts can lag by 24–48 hours—and often land in a generic “operations” inbox, delaying resolution even longer.

5. The Ripple Effects: Higher DSO, Cash-Flow Volatility, and Stakeholder Friction

When payments drag on, the knock-on impacts can undermine your entire finance function:

- Days Sales Outstanding (DSO) Bloat: Suppliers and channel partners waiting on funds may delay their own shipments, pushing your receivables timeline further out. A 5-day average delay on 100 invoices per month can spike DSO by more than a week.

- Unpredictable Cash Flow: Without real-time visibility, forecasting becomes guesswork. You may find yourself over-reserving cash “just in case,” or scrambling to cover unexpected shortfalls.

- Supplier & Employee Dissatisfaction: Late supplier payments can jeopardize volume discounts, while delayed payroll in a new market can erode trust with local hires, undermining your employer brand.

Key Takeaway: Traditional cross-border payments introduce hidden drag at every step, from multiple banking hops and fee stacking to manual compliance checks and opaque transaction status. By quantifying these costs in days, basis points, and headcount, finance leaders can build a compelling business case for automation and transform a leaky, unpredictable process into a competitive advantage.

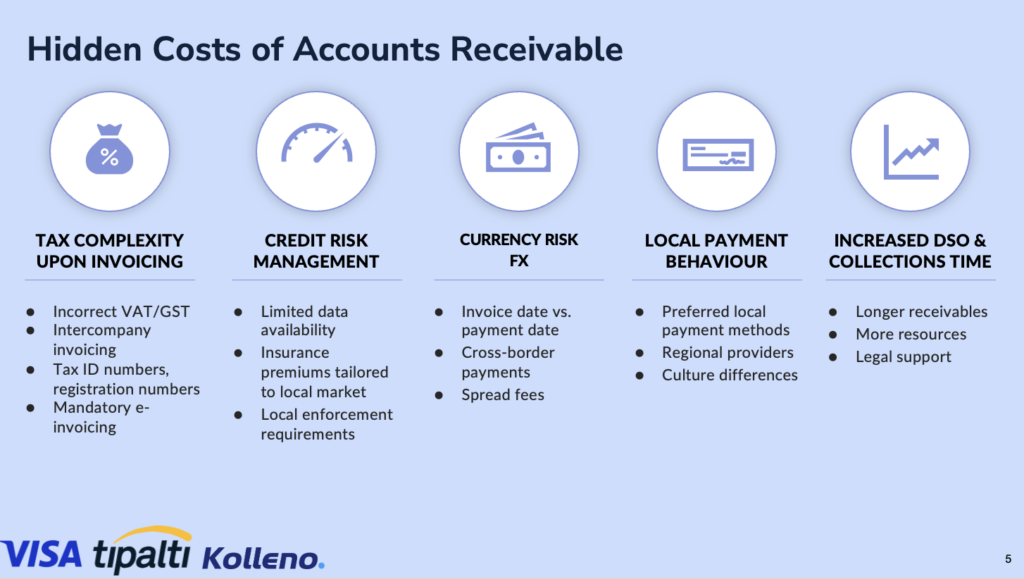

Challenges in Accounts Receivable & Payable and How to Mitigate Them

Cross-border AR and AP introduce hidden layers of complexity that go far beyond simple currency conversion.

1. Tax Complexity upon Invoicing

Every market has its own indirect tax regime—VAT in Europe, GST in APAC, provincial sales taxes in Canada, and so on. When you invoice internationally, you must:

- Determine the correct tax treatment for goods vs. services, digital vs. physical products, and B2B vs. B2C customers. Rates and exemption rules can vary not only by country but by service type.

- Register for tax IDs in each jurisdiction where you have taxable presence, which often entails local filings and renewal obligations.

- Generate mandatory e-invoices in the prescribed digital formats (e.g., PEPPOL in the EU, CFDI in Mexico), and submit them to local authorities within strict deadlines—failure can trigger fines or blocked transactions.

- Ensure intercompany invoicing compliance so that cross-border transfers between your own entities carry the correct tax codes and reconciliation references.

2. Credit Risk Management

Entering a new market often means you lack robust credit data on local customers, leading to:

- Limited data availability, which forces you to rely on third-party credit bureaus (often costly) or manual assessments that delay approvals.

- Higher insurance premiums for trade credit insurance when covering receivables in emerging markets, sometimes adding 0.5–1% of invoice value to your cost base.

- Varying legal enforcement frameworks—what’s easy to collect in Germany may be nearly impossible in certain jurisdictions, lengthening dispute resolution from weeks to months.

Mitigation Tip: Use dynamic credit limits that adjust based on real-time payment behavior, and negotiate pre-approved insurance terms before launching in a new country.

3. Local Payment Behaviors

Customer expectations and banking infrastructures differ widely:

- Preferred methods: SEPA Credit Transfer dominates Euro-zone B2B, BACS is standard in the U.K., while many U.S. enterprises still rely on ACH.

- Regional providers vs. global networks: A local rails specialist may offer lower fees and faster settlement, but integrating multiple providers increases technical overhead.

- Cultural norms: In some markets, 60-day payment terms are standard; in others, Net-30 with dynamic discounting for early payment is the norm. Failing to adapt can strain customer relationships and impede cash flow forecasting.

Case in Point: A U.K. exporter discovered only 10% of its German clients would adopt SWIFT; the rest insisted on SEPA mandates, forcing dual-rail connectivity that added both licensing fees and middleware complexity.

4. Increased DSO & Collection Times

Cross-border receivables often take longer to collect due to:

- Longer dispute resolution: Language barriers and local holiday calendars can extend resolution cycles by 2–3× versus domestic disputes.

- Time-zone mismatches: A simple clarification call may take days to schedule, pushing cash inflows further out.

- Legal costs: Engaging local counsel for overdue receivables can cost 5–10% of the invoice value, quickly offsetting any benefit from late-payment penalties.

Quantifying the Drag: If your average invoice is $25,000 and DSO creeps up by just 7 days on 100 invoices monthly, your working capital requirement increases by $1.75 million—and at a 10% annual cost of capital, that’s roughly $4,800 per month in financing expenses alone.

5. Accounts Payable: Manual Matching & Multi-Currency Headaches

On the AP side, teams face:

- Manual invoice matching, where 3-way checks (PO, receipt, invoice) across different currencies become error-prone and time-intensive.

- Multi-currency pay-runs that require constant FX lookups, leading to mismatches between invoiced amounts and paid amounts—and creating reconciliation nightmares.

- Audit risks, as decentralized payment processes and spreadsheets make it difficult to demonstrate clean controls over every step.

Action Step: Automate invoice ingestion with OCR and AI-driven matching rules, and centralize FX management so every pay run leverages pre-negotiated rates and hedge positions.

By diving deep into these AR/AP complexities—tax rules, credit risk, payment behavior, collection lags, and manual AP toil—finance teams can quantify the hidden drag on working capital, headcount, and compliance. The next step is to deploy an integrated finance automation platform that codifies local rules, applies real-time risk scoring, and provides end-to-end visibility, transforming a leaky process into a scalable competitive advantage.

Deep Dive: Mitigating Risks through Finance Automation

When it comes to cross-border growth, automating your financial operations isn’t just a “nice-to-have”—it’s mission-critical. A purpose-built automation platform acts as a central nervous system for your global payments, foreign exchange, and tax workflows, turning manual toil into seamless, audit-ready processes.

1. Manage Currency Fluctuations

Automated Forward Contracts & Hedging

Rather than leaving every payment at the mercy of spot rates, top platforms let you set up forward-contract rules that lock in exchange rates for future invoices. You can define thresholds—e.g., “hedge when GBP/USD moves beyond ±1%”—and the system executes the contract automatically, preserving your margins without manual intervention.

Dynamic Rate Aggregation

By pooling transaction volume across all subsidiaries, an automated solution can aggregate FX needs and negotiate institutional-grade rates with multiple liquidity providers in real time. This collective scale often delivers better spreads than any single entity could secure on its own.

Proactive Alerts & Reporting

Rather than reacting to rate swings after the fact, dashboards can alert treasury teams when market volatility spikes, enabling quick decisions on pre-hedging or invoice timing. Custom reports show your exposure by currency pair, maturity date, and counterparty—giving you the data to refine your FX policy continuously.

2. Minimize FX Risks

Real-Time Conversion at Point of Payment

Manual FX conversions can introduce delays and errors. Automation platforms connect directly to banking APIs, executing conversions at the moment of payment initiation and capturing the precise rate, timestamp, and reference details—all logged for audit.

Automated Netting & Multilateral Settlement

When you have receivables and payables across the same currencies or counterparties, software-driven netting can offset positions automatically, reducing the number of transactions, cutting fees, and lowering settlement risk.

Error-Proof Execution

Pre-configured business rules prevent out-of-policy trades—e.g., flagging any conversion above a set threshold or blocking transactions against embargoed jurisdictions—ensuring consistency even as volumes grow.

Integrated Tax & Customs Engines

Rather than maintaining spreadsheets of duty rates, an embedded tax engine automatically calculates the correct tariff classification (HS codes), duty rates, VAT/GST, and any regional surcharges based on product attributes and destination.

Seamless E-Invoicing Compliance

Platforms can generate and transmit e-invoices in local formats—whether PEPPOL in the EU or CFDI in Mexico—meeting government mandates without manual rework.

Automated Tax Filings & Remittances

Beyond invoice creation, the same system can schedule VAT/GST returns, prepare XML filings, and even remit collected taxes to local authorities, reducing the risk of penalties or late-filing fees.

4. Scale Payments without Headcount

Configurable Approval Workflows

As your payee network grows, building one-off approval chains becomes untenable. Automation platforms let you define rules (e.g., “all invoices > $50,000 require CFO sign-off”) that apply globally or by region, instantly routing requests to the right stakeholders.

Self-Service Vendor Onboarding & KYC

A secure portal allows suppliers to submit their banking details, tax forms, and compliance documentation directly. Automated data validation and integration with global watch-lists accelerate KYC reviews and reduce back-and-forth with finance teams.

Batch Payments & Bulk Runs

Whether you’re paying 50 or 5,000 vendors, a single click can launch a multi-currency pay-run. The system handles format conversions (e.g., SEPA XML vs. Fedwire), bank connectivity, and exception management—meaning no extra hires as your payment volume scales.

5. Ensure End-to-End Visibility

Unified Payment Dashboard

Instead of toggling between ERP, banking portals, and spreadsheets, finance leaders get a single pane of glass showing every payment’s status: approved, submitted, in transit, or settled.

Drill-Down & Exception Alerts

Failed or delayed payments trigger real-time notifications, complete with root-cause diagnostics (e.g., invalid IBAN, sanctions hit, or insufficient funds), so teams can resolve issues before they impact suppliers or employees.

Comprehensive Audit Trail

Every action, from user login and approval timestamp to API call logs, is recorded and time-stamped. Built-in reporting exports ensure you can satisfy internal auditors and local regulators without manual reconciliation.

Advanced Action Plan for Finance Leaders

- Conduct a Process Maturity Assessment

Map your current payment, FX, and tax workflows against industry best practices to identify quick wins (e.g., e-invoicing) and long-term projects (e.g., integrated hedging). - Build a Cross-Functional Task Force

Involve treasury, tax, IT, and procurement early to align on requirements, data sources, and integration priorities. - Pilot with High-Volume Corridors

Start automation in your top 2–3 currency pairs or regions where costs and risks are greatest, then scale globally once ROI is proven. - Define Success Metrics & SLAs

Track KPIs such as FX spread reduction, average days to settle, headcount savings, and compliance error rates—review them in your monthly finance-ops cadence. - Iterate & Expand

After stabilizing core AP/AR and FX, layer in advanced use cases like multilateral netting, dynamic discounting, and AI-driven anomaly detection to continuously drive efficiency.

By embedding these automated capabilities into your financial backbone, you not only plug the hidden “leaks” in cross-border operations but also turn global payments into a strategic lever, enabling faster market entry, improved supplier relationships, and measurable cost savings.

Conclusion: Turn Hidden Costs into Strategic Wins

International expansion may promise new customers, prestige, and growth, but it also introduces a labyrinth of hidden costs that can quietly drain your margins and stall your momentum. From fragmented payment rails and FX inefficiencies to regulatory landmines and AR/AP delays, the financial drag is real and growing with each new market you enter.

The good news? With the right finance automation strategy, these challenges become not just manageable, but an opportunity for competitive advantage. By streamlining cross-border payments, enforcing tax compliance, mitigating FX risk, and increasing visibility across global operations, CFOs and finance leaders can shift from firefighting to future-proofing.

As shared in our webinar with Visa and Tipalti, the key is not just expansion—but smart expansion. And that starts with modernizing your finance stack to support scalable, secure, and insight-driven global operations.