The first step to ensuring the viability of your company’s finances is to understand your cash flow. Cash flow, the amount of money that flows in and out of your business over a given period, is a good indicator of financial health.

It’s important to understand cash flow key performance indicators (KPIs) to ensure that you have sufficient funds for your business to grow and pay your bills. A company’s cash flow metrics help to measure its performance. In addition to helping you make decisions, these metrics help assess the quality of newly implemented practices, while investors also use this information to compare companies.

Dive into our article to learn everything you need about cash collection metrics and formulas.

KPIs for cash collections

The debt collection process is about getting invoices paid. It consists of monitoring collections and making necessary reminders to recover your customer receivables quickly and keep up cash inflows. The company can carry out these operations or entrust them to a collection agency. In both cases, it’s worth looking at the actions’ performance. If collection is managed in-house, analysing the performance of operations facilitates team management and can alert you to the need to review your procedures. If a collection agency is involved, it’s also a good idea to monitor the actions taken and have indicators at your disposal to ensure effective cash flow management.

Several KPIs are available to companies to analyse the efficiency of their cash flow processes. Some, such as DSO, are used at all company levels (operational and management). Others are more useful for managers: credit managers, administrative and financial directors, etc. We selected ten key operating cash flow indicators and KPIs you can regularly monitor throughout their annual operations. Here are 13 indicators and formulas to look into to streamline debt collection management within your organisation.

Let’s note that PWC’s guide to key performance indicators does not specify a number of KPIs or a specific template to implement, rather stating that “experience suggests that between four and ten measures are likely to be key for most types of company”.

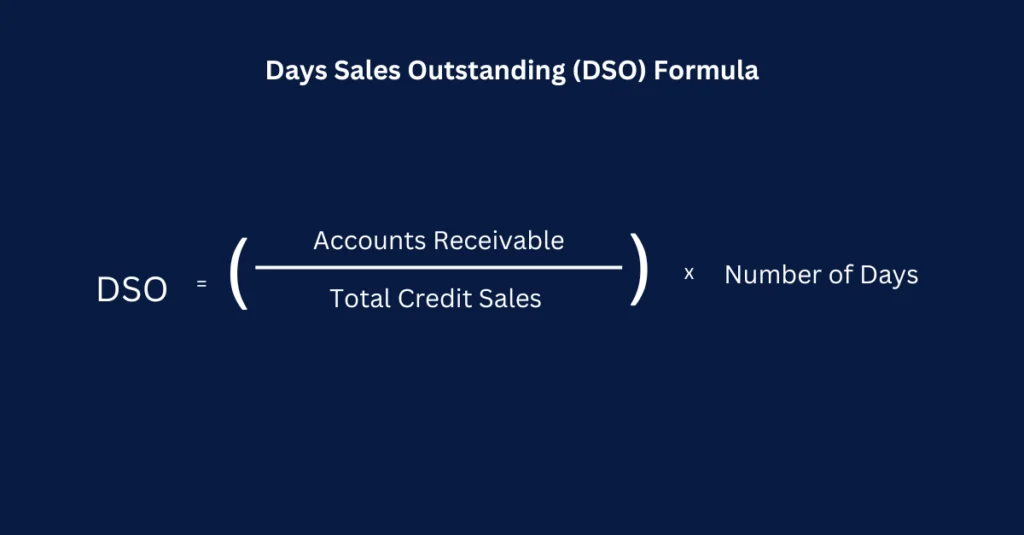

1. Days Sales Outstanding (DSO)

DSO represents the average days required to collect payments following a credit sale. It’s also called “Average debtor days”. The average debtor collection period formula can be found by dividing the average daily sales by the average debtor days. “Average debtor days” refer to the median days between issuing invoices and collecting payments owed from a client or customer.

Regarding cash conversion cycles, a low DSO or low average debtors collection period indicates that you can quickly collect receivables from your customers. High DSO can indicate poor collection practices and cash flow problems.

The DSO formula is pretty straightforward: it’s your Accounts Receivable at the end of the period divided by your gross sales over the same period. You then multiply this number by the number of days in the period. It’s essential to have a solid debtor collection period interpretation to make sure you can assess and pivot your strategy if needed.

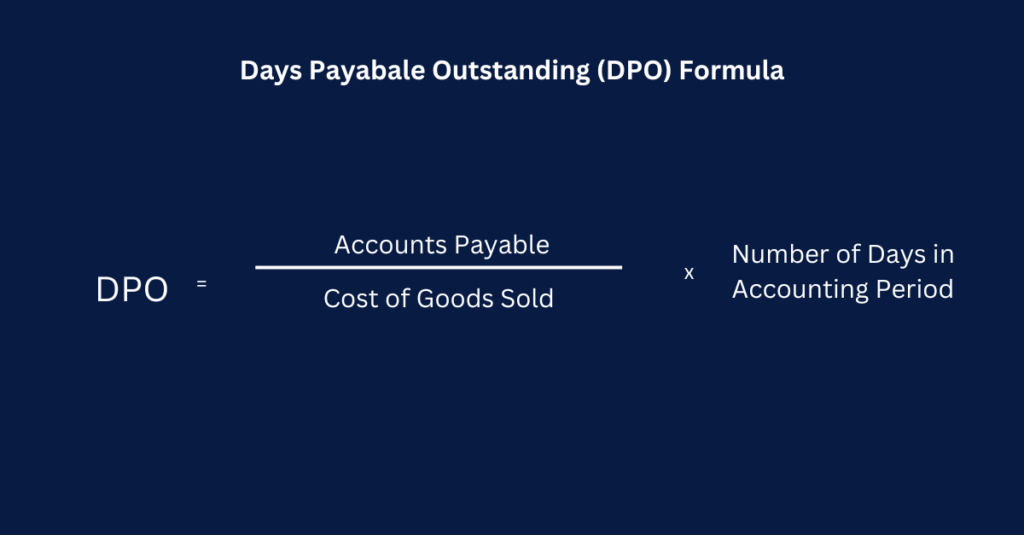

2. Days Payable Outstanding (DPO)

DPO is the inverse of DSO. It measures the average time it takes a company to pay its suppliers. The formula is as follows: Accounts Payable x Number of Days in accounting period / Cost of Goods Sold (COGS)

As a result, if you have a high DPO, you can hold cash longer and invest it in the short term for higher returns. However, a very high OPD may also indicate that your credit conditions may be at risk in the future. If your DPO is low, this suggests that your company is not taking advantage of available credit terms or negotiating better terms. Like DSO, DPO can vary from one sector to another. However, a period of around 30 days for creditors is generally considered an excellent OPD.

3. The Aged Trial Balance (ATB)

Very useful for securing cash flows, the Aged Trial Balance (ATB) summarises trade receivables and payables at a given time. Particularly useful from an operational point of view, it shows the total amount of outstanding receivables and enables you to prioritise your reminders. This means better informed decisions and financial planning.

The aged trial balance takes a tabular form and shows the amounts due, customer by customer, broken down into different columns according to invoice status: not yet due, less than 30 days overdue, 30 to 60 days, 60 to 90 days, 90 to 120 days overdue, and so on.

This management tool enables debt collectors to monitor invoice payments. In the event of late payment, the aged trial balance is also used to organise any reminders or legal proceedings required to recover receivables and avoid cash flow problems. You can also use aged trial balance figures to measure your DSO and another complementary collection performance indicator: Average Days Delinquent, the calculation formula explained below.

4. Average Days Delinquent (ADD)

ADD is the average number of days your invoices are overdue. As a reminder, late payment occurs the day after the payment due date. The default payment term of 30 days can be extended to 45 or even 60 days at the end of the month, depending on the sector or following a commercial agreement.

ADD is an essential indicator for collection departments. The higher your ADD, the longer it takes for your customers to pay you. If it increases, your collection teams need to redouble their efforts and increase the frequency of reminders, especially for customers with the highest ADD.

5. Accounts Receivable Turnover (ART)

Accounts receivable turnover rates provide insight into a company’s collection efficiency. You can calculate it by dividing net credit sales by average accounts receivable over a period.

It measures the frequency with which receivables are converted to cash over a given period. It’s also known as the accounts receivable turnover rate. Companies with a high ART are better able to collect their receivables. Companies with a low ART either find it difficult to collect their receivables or offer their customers overly lenient payment terms.

However you also need to consider your collection period formula to calculate your collection period. The average collection period ratio is closely intertwined to your accounts receivable turnover ratio. Indeed, the turnover ratio indicates how often you collect your accounts, while the collection period ratio tells you how long it takes to collect cash. The ar collection period formula is easy to use.

Using this calculation, you discover how long it takes to collect from when the invoice is issued to when you get paid. If the average is low, it’s good. You collect accounts relatively quickly. An increasing average receivables collection period indicates trouble collecting your accounts. A high average collection period ratio could indicate trouble with your cash flows.

The accounts receivable collection period formula is Days x Average Accounts Receivable / Net Credit Sales = Average Collection Period Ratio.

6. Collection Effectiveness Index (CEI)

The Collection Effectiveness Index (CEI) is also a key indicator for measuring the operational efficiency of the system collecting trade receivables. This collection formula corresponds to the ratio between the number of receivables collected during a given period and the amount to be recovered over the same period. This indicator concerns the teams in charge of customer receivables: accounting and collection departments, finance departments, etc. A drop in the CEI is an early warning of a future cash flow problem and indicates the need to remobilise teams or review collection organisations.

7. Bad Debt to Sales Ratio

Bad debt to sales ratio refers to the percentage of your company’s bad or doubtful debts in regard to sales. It’s essential to look into this ratio to assess and improve your collections. It can be used to establish your collection risk management policy, important for making smart strategic decisions.

8. Accounts payable turnover (APT)

A company’s accounts payable turnover rate, also known as its creditor turnover rate, measures short-term liquidity and indicates the frequency with which it pays its creditors.

A high APT may indicate that your company is not using its credit facilities effectively or that your suppliers are not granting you favourable credit terms. A lower APT indicates that your credit lines are being used effectively. However, a very low APT can cause friction in your relationships with your suppliers. It’s always worth comparing this value with other sector companies and supplier payment terms.

9. Current Ratio

The current ratio reflects the relationship between current assets and current liabilities. It indicates the extent to which a company can repay its short-term obligations.

The higher the rate, the more likely the company is to be able to repay its loans in the short term. A low rate may indicate future difficulties in paying its bills. Consequently, accounts receivable with a current low rate are likelier to see their open invoices turn into bad debts.

Having a current ratio between 1.5 and 3 is generally considered healthy. When the current ratio is 2, the company has twice the amount of cash or assets to cover its short-term obligations.

10. Free cash flow (FCF)

A company’s free cash flow is used to repay creditors, pay interest and distribute dividends. The cash available to a company after it has paid its short-term debts and invested in operating equipment is called working capital.

A company with a high FCF indicates good operating cash flow and surplus cash available to make new investments, repay debts or pay dividends.

11. Cash Flow Coverage Ratio (CFCR)

A company’s CFCR indicates whether cash flow from operations can cover its debt obligations. In other words, it’s the operating cash flow ratio to total debt.

If the CFCR is high, the company is in a good position to repay its debts. Companies should have a cash flow coverage ratio of at least 1.5. For example, a cash flow coverage ratio of 1.5 means a company has $1.5 operating cash flow to cover $1 of interest expense.

A cash flow coverage ratio inferior to 1.5 may indicate the company has poor debt management practices or difficulty making interest payments on time.

12. Cash Conversion Cycle (CCC)

A company’s cash conversion cycle, also known as the net operating cycle, measures the time required to convert inventories and investments into cash. This time is measured in days.

It measures the time required for each dollar invested in production and sales processes to be converted into cash payments. This analysis considers the time the company takes to sell its inventories, collect its receivables and pay its invoices. If the CCC is lower, the company is more likely to be able to collect payments quickly.

13. Forecast Variances

Forecast variances measure the difference between your cash flow forecasts and actual results. Companies need to monitor the difference between their forecast and actual cash flows to determine the accuracy of their estimates.

You can make better business decisions by tracking forecast variations over a given period. The higher the forecast variations, the less likely you are to use the correct variables in your model or to have to modify the input parameters. The lower they are, the stronger the predictive capability and the greater the decision-making capacity.

How do you choose the right financial KPIs for your company?

To optimise resources, you’ll need to choose the right metrics to track the effectiveness of operating cash flows. However, this can be a difficult task. The following tips will help you select your organisation’s best cash flow indicators.

Don’t measure everything

If you try to track every financial indicator, you’ll only confuse yourself and won’t be able to focus on the most important ones. Identify the indicators you want to track according to your business objectives and the impact you want to achieve. To reduce debt by 50% over the next two years, you should monitor FCF, current rate and FCFR.

Do the KPIs give you the whole picture?

Once you’ve chosen a set of operating cash flow KPIs to track, periodically assess whether they give you a complete picture of what you’re looking for. If they don’t, you must consider which metrics must be added to your tracking tool and which can be removed. It’s important to re-evaluate the metrics you track as your business objectives evolve.

Seek external consultation

Consult third-party experts to review your business operations if your company doesn’t have sufficient financial resources or expertise to set up trackers and dashboards to monitor your most relevant financial metrics.

Automate the process with software solutions

Software solutions such as Toucan enable you to integrate data from multiple sites and track the most relevant treasury metrics. Using automation tools provides real-time data and visual representations of key metrics. On the contrary, manual monitoring of operating cash flow indicators does not allow you to receive real-time updates. Using poor-quality data to monitor operating cash flow KPIs can harm your company’s day-to-day operations and investment plans. As a result, stakeholders will also be impacted. Monitor operating cash flow KPIs using analytics tools while optimising your accounting, accounts receivable and cash management operations.

According to PYMENTS’ report on automation, more than 70% of businesses reported that automation leads to improved cash flow, increased savings, and overall business growth. Today, CRM and other digital tools offer various functionalities to optimise billing and collection operations. For better management of your accounts receivable, remember to consult them regularly and to monitor them over time to detect any signs of weakness, whether they are cash management.

Final thoughts

All businesses depend heavily on cash flow. According to a survey from QuickBooks, three in five UK small business owners are experiencing problems with their companies’ cash flow. Tracking KPIs and indicators using the right collections performance formula related to operating cash flow is essential to avoid problems with cash balance, debt and even bankruptcy. Having all the information they need in real-time (for example, in a cash flow statement) is vital for collection teams.

To effectively monitor payments, operational staff need to have an overall view of outstanding receivables and be able to edit an aged trial balance easily. To monitor activities and check the effectiveness of collection procedures, managers need access to collection performance indicators such as DSO (Days Sales Outstanding), Average Days Delinquent (ADD), Collection Effectiveness Index (CEI) and many other KPIs (receivables turnover ratio, percentage of bad and doubtful debts, cash conversion cycle, etc.).

- KPIs for cash collections

- 1. Days Sales Outstanding (DSO)

- 2. Days Payable Outstanding (DPO)

- 3. The Aged Trial Balance (ATB)

- 4. Average Days Delinquent (ADD)

- 5. Accounts Receivable Turnover (ART)

- 6. Collection Effectiveness Index (CEI)

- 7. Bad Debt to Sales Ratio

- 8. Accounts payable turnover (APT)

- 9. Current Ratio

- 10. Free cash flow (FCF)

- 11. Cash Flow Coverage Ratio (CFCR)

- 12. Cash Conversion Cycle (CCC)

- 13. Forecast Variances

- How do you choose the right financial KPIs for your company?

- Final thoughts