DSO Reduction Software: How to Reduce Days Sales Outstanding Faster

Discover how DSO reduction software can transform your cash flow.

Learn more

Centralize AR data, automate follow-ups, and track payments. Replace spreadsheet chaos with one streamlined platform.

Make it easier for clients to pay you securely and on time. Centralize all payment options in one portal to remove friction and accelerate cash flow.

Streamline payment matching, posting, and tracking. Automate complex reconciliation scenarios to free your team from manual data entry.

Rakuten ditched manual workflows. See how Kolleno's multi-agent workforce took over the heavy lifting to accelerate cash flow.

See case study

When a $4.1B software giant needed to scale, they upgraded to Kolleno. See how our multi-agent workforce executes the heavy lifting.

See case study

See how Drata unified their collections with smart automation, empowering 100+ users to drive down past-due balances by 96%.

See case study

Discover how DSO reduction software can transform your cash flow.

Learn more

Discover proven strategies to collect past due accounts effectively. Learn communication tips, legal boundaries, and when to escalate.

Learn more

Learn what the average collection period is, how to calculate it, and actionable strategies to improve your cash flow.

Learn more

Learn what a dunning letter is, how to write one, and get templates for every stage of the collections process.

Learn more

Master DSO in finance. Learn how to calculate Days Sales Outstanding, interpret results, and reduce collection cycles.

Learn more

Discover how DSO reduction software can transform your cash flow.

Discover proven strategies to collect past due accounts effectively. Learn communication tips,

Learn what the average collection period is, how to calculate it, and actionable strategies to

Learn what a dunning letter is, how to write one, and get templates for every stage of the coll

Master DSO in finance. Learn how to calculate Days Sales Outstanding, interpret results, and re

Learn how aging accounts receivable reports work, what the numbers mean, and how to act on them

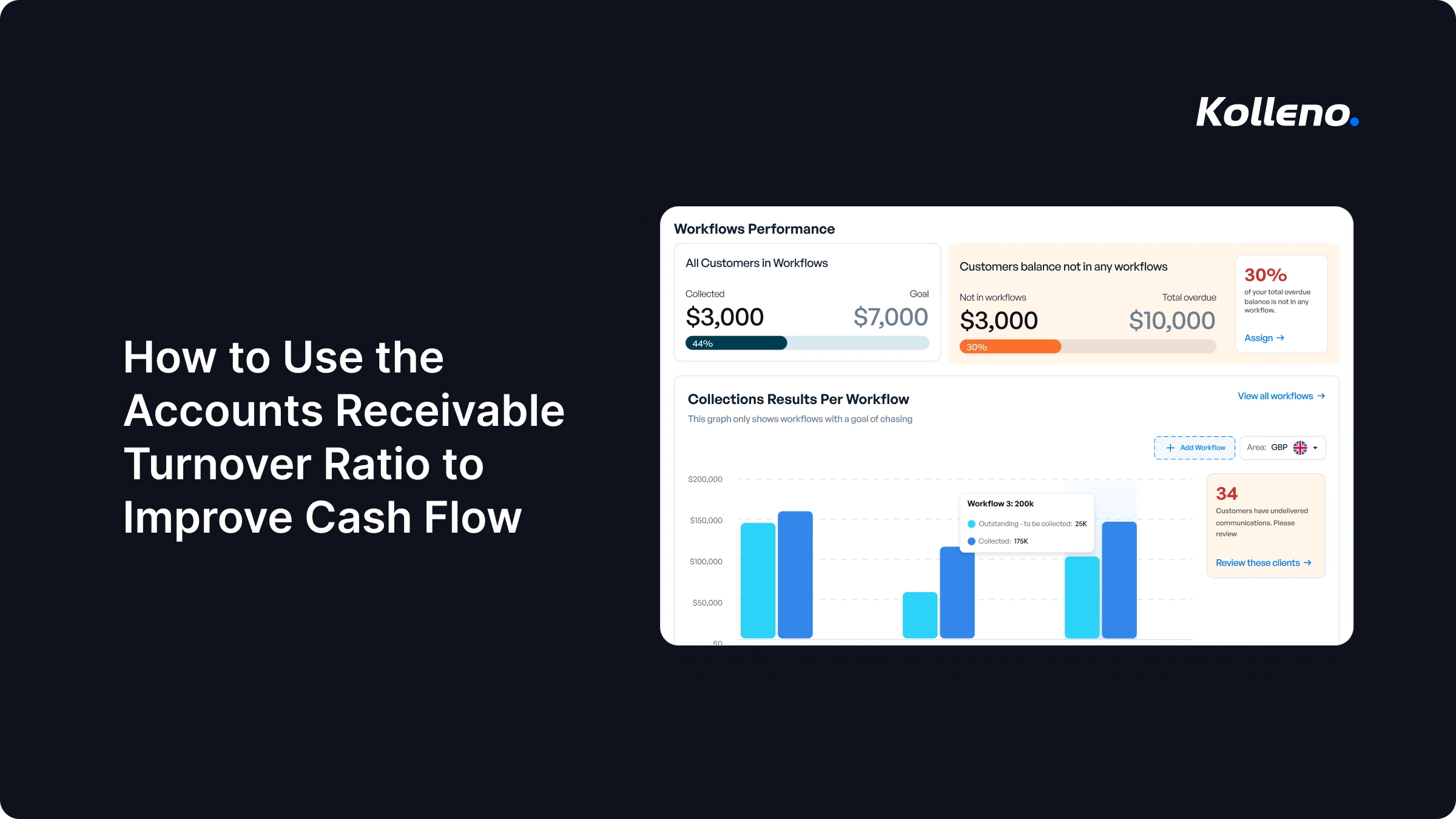

Learn how to calculate the accounts receivable turnover ratio.

Learn how accounts receivable automation reduces DSO, eliminates manual tasks, and improves cas

Master accounts receivable management.