Finance teams know AR management matters. The challenge is execution: invoices go out, follow-ups get delayed, and cash flow becomes hard to predict.

In this guide, we’ll cover:

- What accounts receivable management covers

- The core AR process, step by step

- Key metrics and how to interpret them

- Best practices for optimizing your AR function

- Common challenges and how to address them

What Is Accounts Receivable Management?

Accounts receivable management is the set of processes a business uses to ensure it collects payment for goods and services it has already delivered. It covers everything from establishing credit terms at the point of customer onboarding through to cash reconciliation when payment arrives.

Effective AR management directly affects liquidity, working capital, and profitability. A business can grow quickly and still run into cash flow pressure if receivables lag. Conversely, a disciplined AR function reliably converts sales into cash and gives finance leaders visibility into what’s coming in and when.

The AR cycle includes credit management, invoicing, collections, dispute resolution, and reporting, and each stage affects the next.

The Core Accounts Receivable Process

Step 1: Credit Policy and Customer Onboarding

Before extending credit to a customer, you need to assess their creditworthiness. This means reviewing payment history, financial stability, and the size of the credit line you’re prepared to offer. A documented credit policy keeps credit decisions consistent and independent of whoever owns the account.

Clear payment terms should be established and communicated at onboarding. Net 30, Net 60, or milestone-based payment structures all have implications for your cash conversion cycle. Whatever you agree, make sure it’s in the contract and on every invoice.

Step 2: Invoicing and Billing

Invoice accuracy matters more than most teams acknowledge. Errors in amounts, dates, or purchase order references are a leading cause of payment delays. Customers use invoice discrepancies as a reason to hold payment until the issue is resolved, which can add weeks to your DSO.

Invoices should go out promptly after delivery and include everything the customer’s accounts payable team needs: line items, payment instructions, bank details, and any reference numbers required by their system. Electronic invoicing reduces delivery delays and creates a logged record of when the invoice was received.

Step 3: Payment Processing and Cash Application

When payments arrive, they need to be matched to the correct invoices quickly and accurately. Unapplied cash distorts your AR balance and creates confusion when customers query their account status. Cash application involves reconciling payment amounts against open invoices, accounting for partial payments, and flagging discrepancies for resolution.

Step 4: Collections and Follow-up

Collections is not a single action. It’s a sequence that escalates progressively. A friendly reminder before a due date is appropriate. A firm follow-up a week after the due date is also appropriate. By the time an invoice is 60 or 90 days overdue, the tone and communication channel should reflect the seriousness of the situation.

Maintaining customer relationships during the collections process requires professional, consistent communication. Aggressive or inconsistent outreach damages relationships without improving collection rates. Documented, systematic follow-up sequences produce better outcomes.

Key Metrics in Accounts Receivable Management

Days Sales Outstanding (DSO)

Days sales outstanding measures how long it takes, on average, to collect payment after a sale. The formula is: (accounts receivable/total credit sales) x number of days.

A falling DSO usually signals faster collections and better working capital efficiency.

Benchmark against your industry and your own historical performance to put the number in context.

Accounts Receivable Turnover Ratio

This ratio measures how often receivables are converted into cash within a period. Higher is generally better. A low ratio indicates that customers are taking longer to pay or that credit is being extended to customers who represent a collection risk.

Aging Report Analysis

An AR aging report categorizes outstanding invoices by how long they’ve been outstanding: current, 1-30 days, 31-60 days, 61-90 days, and 91+ days. Older buckets carry a lower collection probability. Regular aging report reviews help you prioritize collection effort and identify accounts that need escalation.

Bad Debt Ratio

The bad debt ratio is the percentage of uncollectible receivables to total credit sales. A rising ratio indicates a problem with credit policy, collections effectiveness, or the quality of your customer base. Many finance teams use an allowance for doubtful accounts based on historical bad-debt rates.

Best Practices for Managing Accounts Receivable

Implement a Clear Credit Policy

A written credit policy removes inconsistency from credit decisions. It should define the criteria for extending credit, how credit limits are set, what payment terms are available, and under what circumstances credit is withheld or reduced. Apply it consistently across every customer, regardless of relationship history or deal size.

Optimize Invoicing and Payment Terms

Send invoices through the channels your customers actually use. Electronic invoices delivered to the correct contact are processed faster than paper invoices sent to a generic AP email address. Payment portals that accept multiple payment methods reduce friction. Early payment discounts can accelerate cash collection when the discount’s cost is offset by the benefit relative to your cost of capital.

Communicate Proactively

Send a reminder before the due date, not just after it. Customers who receive a polite advance notice pay more consistently than those who only hear from you when a payment is already late. Proactive communication also surfaces disputes earlier, giving you time to resolve them before they delay payment.

Standardize Dispute Resolution

Disputes that sit unresolved hold up payment on the entire invoice or a portion of it. A defined dispute resolution process, with clear ownership and response timeframes, shortens resolution cycles and reduces the number of disputes that escalate into write-offs.

Use Technology and Automation

Manual accounts receivable management processes break down as invoice volume increases. As invoice volumes grow, so does the risk of delays, errors, and missed follow-ups. AR automation platforms handle invoicing, reminders, cash application, and reporting consistently, without relying on individual team members to remember to act. The result is a more reliable process and more time for your AR team to focus on the accounts that genuinely need human attention.

Monitor KPIs Consistently

AR metrics are only useful if you review them regularly and act on what they show you. A quarterly DSO review is usually too slow to catch emerging collection issues. Reviewed weekly, DSO becomes a useful management signal. Build regular AR reporting into your finance team’s rhythm and use it to drive decisions about credit, collections, and process improvement.

Common Challenges in Receivables Management

Late payments are the most visible challenge, but they’re often a symptom of earlier process failures: unclear payment terms, delayed invoicing, or credit extended to customers already at risk of collection. Addressing the root cause matters more than intensifying the collection effort on invoices that are already overdue.

Lack of visibility is another persistent problem. When AR data is spread across spreadsheets, email threads, and ERP records that don’t communicate cleanly with one another, finance leaders can’t see what’s actually outstanding or where the collection risk lies. Centralizing AR data and automating reporting resolves this.

High bad debt rates typically point to a credit policy that is either too permissive or applied inconsistently. Tightening credit criteria and enforcing them systematically reduces bad debt exposure, even if it means declining credit for some customers in the short term.

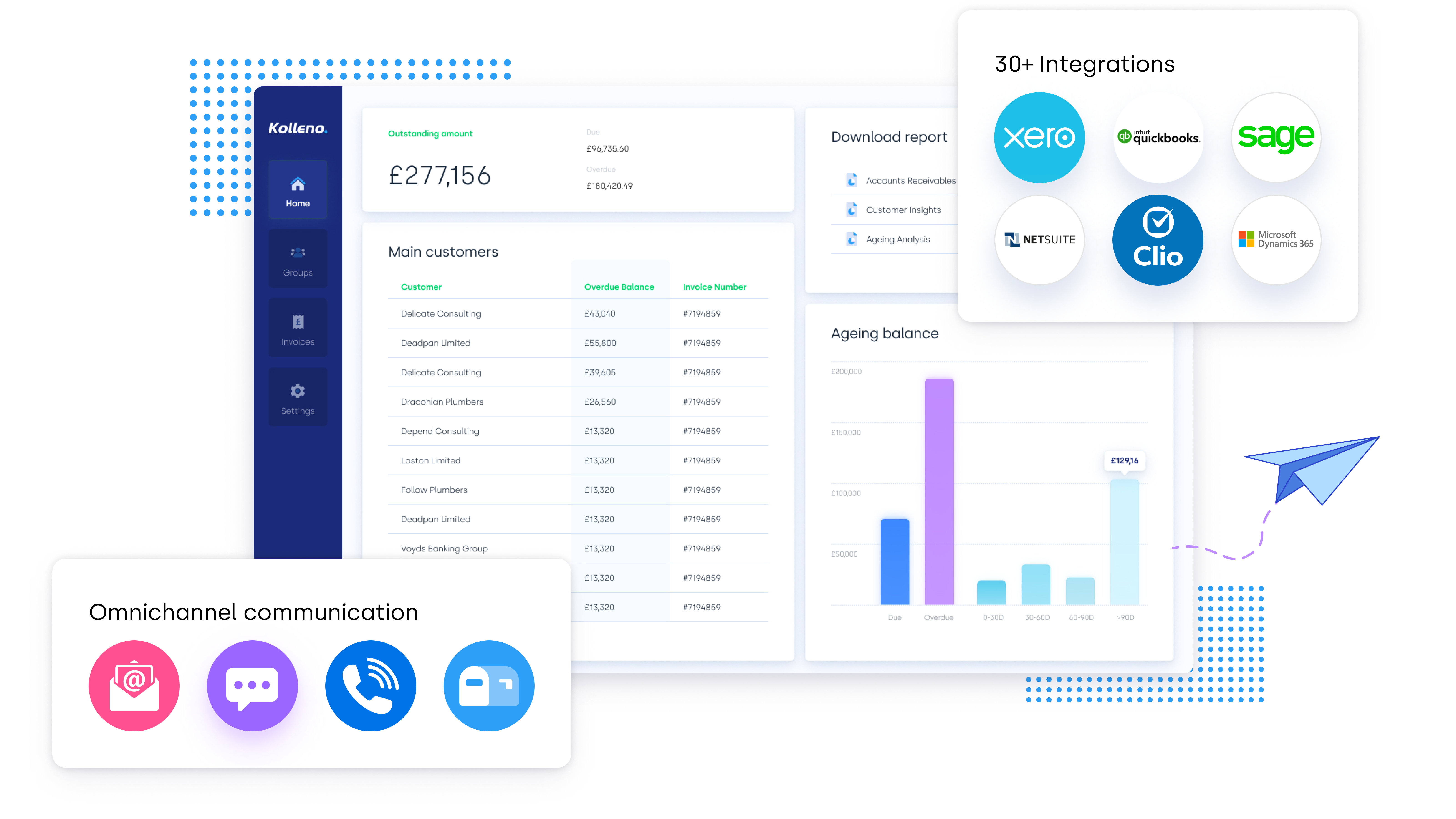

How Kolleno Fits Into the AR Process

Kolleno’s O2C platform uses a Multi-Agent AI Workforce to orchestrate collections, route disputes, accelerate cash application, and monitor credit risk in line with the policies your team sets. Finance teams configure the credit policy and collection rules, and Kolleno’s AI Agents streamline the execution across every account, at scale.

The platform integrates with major ERPs and CRM systems, keeping AR data current and actionable without manual exports. Finance leaders get real-time visibility into aging balances, payment risk, and collection performance, while the AR team focuses on the accounts and decisions that actually require their expertise.

Final Thoughts

Accounts receivable management is not a back-office function. It’s a direct driver of cash flow, working capital, and financial predictability. The teams that manage accounts receivable well combine clear credit policies, consistent execution, and the right technology to handle volume without losing visibility.

If you want to see how Kolleno supports this across the full order-to-cash cycle, book a demo today.

Frequently Asked Questions

What is the difference between accounts receivable and accounts payable?

Accounts receivable is money owed to your business by customers for goods or services already delivered. Accounts payable is money your business owes to suppliers for goods or services it has received. Both affect working capital but in opposite directions. Efficient AR management shortens the time money spends as a receivable and improves cash flow.

What is a good DSO benchmark?

DSO benchmark ranges vary by industry, contract value, and payment terms. The most useful baseline is your own payment terms: if you offer Net 30 and your DSO is 45, that gap deserves investigation.

How often should you review your AR aging report?

Weekly is the minimum for any business with meaningful invoice volume. High-volume operations benefit from daily or real-time visibility. Monthly reviews are insufficient because issues identified at month-end have already had weeks to compound. Frequent review enables earlier intervention for at-risk accounts and reduces the likelihood of invoices progressing into the oldest aging buckets.

When should you write off a bad debt?

The decision to write off a bad debt depends on the age of the invoice, the amount outstanding, the cost of further collection effort, and the probability of recovery. Most businesses apply an aging policy: overdue accounts that have not responded to escalated collection attempts for over 180 days are strong candidates for write-off. Document all collection activity before writing off any balance.