Accounts receivable collections are not a single conversation. It’s a structured sequence of decisions and actions that begins before an invoice is even issued. Businesses that manage this process well collect more, write off less, and maintain customer relationships throughout the process. Those who don’t often find themselves in constant reactive mode, chasing the same overdue balances without a consistent approach.

This guide explains what the accounts receivable collection process involves, why a structured approach is essential for improving cash flow and reducing bad debt, and the steps involved in an effective collection cycle. It also explores best practices for optimizing collections, common challenges and how to overcome them, the legal considerations surrounding B2B debt collection, and the key performance indicators (KPIs) used to measure collections’ effectiveness.

Why an Effective AR Collection Process Matters

Improve Cash Flow and Working Capital

An efficient accounts receivable collection process directly affects cash flow and working capital. Every day an invoice stays unpaid is a day that cash is not available to fund operations, service debt, or invest in growth. A consistent, well-designed collection process shortens that gap systematically across every customer account, not just the ones that happen to get noticed.

Reduce Bad Debt

Bad debt write-offs are heavily influenced by the quality of your collection process. Invoices that enter collections early, with clear escalation paths, are recovered at significantly higher rates than those left unactioned for months. The cost of a missed follow-up is not just a delayed payment; it increases the risk of the balance becoming uncollectable.

Strengthen Customer Relationships

Professional, consistent collections communication builds more trust than sporadic, urgent contact. Customers who know what to expect from your accounts receivable team are more likely to engage constructively when payment is delayed, helping preserve long-term business relationships while improving collection outcomes.

Common Challenges in AR Collections

Unresponsive Customers

Some customers stop responding to all contact. Before escalating to external agencies, try alternative contacts within the customer organisation, including finance leadership or executive sponsors. A multi-channel approach, combining email, phone, and formal written correspondence, also improves response rates compared to relying on a single channel.

Invoice Disputes

Disputes are one of the most common causes of payment delay. The key is to identify and resolve them quickly. A defined dispute resolution process, with a named owner and a response timeframe, shortens the resolution cycle. Disputes that sit open for weeks become disputes that eventually turn into credit notes or write-offs that could have been avoided with prompt engagement.

Customers with Cash Flow Problems

A customer who genuinely cannot pay in full is a different situation from one who won’t. Payment plans, credit holds, and renegotiated terms may recover money that would otherwise be written off. The priority is to reach a realistic agreement, document it, and enforce it.

The Step-by-Step AR Collection Process

Step 1: Credit Management and Customer Onboarding

The collection process begins at the credit assessment stage, not when an invoice goes overdue. Before extending credit to a new customer, assess their creditworthiness through a combination of credit reports, trade references, and financial history. Define credit limits and payment terms based on this assessment and document them formally.

Payment terms should be explicit: Net 30, Net 60, or milestone-based arrangements all have different implications for your cash conversion cycle. Whatever you agree on, embed it in the contract and display it on every invoice. Ambiguity at this stage creates disputes later.

Customer onboarding should also capture the correct billing contact, invoice delivery preferences, required purchase order references, and any accounts payable platform requirements. An invoice delivered to the wrong person or missing a required reference number will be delayed regardless of what the payment terms say.

Step 2: Accurate and Timely Invoicing

Every day between delivering goods or services and issuing an invoice is a day added to your DSO before the payment clock has even started. Invoice promptly, invoice accurately, and invoice to the right person through the right channel.

Invoice errors are one of the most common causes of payment delays. Incorrect amounts, wrong purchase order references, missing delivery documentation, or VAT treatment errors all give customers a legitimate reason to hold payment while the issue is resolved. Review invoice accuracy as part of your billing workflow, not as an afterthought when a payment dispute arrives.

Step 3: AR Monitoring and Aging Reporting

Once invoices are issued, they need to be tracked. An accounts receivable aging report categorises outstanding invoices by how long they’ve been past their due date. Running this report weekly at minimum gives your AR team visibility into which accounts are approaching or past their due date and where overdue balances are concentrating.

The aging report should drive collection prioritisation. An account with a large balance moving into the 31-60 day bucket from a typically reliable customer is a different priority from a smaller balance in the 91+ day bucket from a repeat late payer. Your collection sequence should reflect these differences.

Step 4: Pre-Due-Date and Due-Date Reminders

A reminder sent before the due date is not a collections action. It’s customer service. Many late payments result not from unwillingness but from invoices that get lost in inboxes, miss the accounts payable processing cycle, or simply require a reminder to trigger payment. A polite reminder three to five days before the due date and a payment confirmation request on the due date itself capture this segment efficiently.

These early reminders should be automated where possible. Manual follow-up at this stage is inefficient and inconsistent. Automation ensures every invoice gets the same treatment regardless of which team member is managing the account.

Step 5: First Follow-Up for Overdue Invoices (1-30 Days Past Due)

When an invoice passes its due date without payment, the first follow-up should be prompt and professional. An email within two to three business days of the due date, acknowledging that payment may have been missed and providing payment instructions, is appropriate at this stage.

If there is no response within a week, a second contact by phone or email is warranted. At this stage, your primary objective is to confirm receipt of the invoice, understand whether there is a query or dispute, and agree on a payment date. Document the contact and any commitments made.

Step 6: Escalation and Negotiation (31-90 Days Past Due)

Invoices that remain unpaid beyond 30 days past due require a more structured escalation. The tone of communication should become firmer while remaining professional. Internal escalation to a senior AR manager or finance director may be appropriate for high-value accounts. Customer-side escalation, reaching out to a senior contact rather than the standard AP contact, can also accelerate resolution.

At this stage, payment plans become relevant for customers who are genuinely unable to pay in full. A structured payment schedule with defined instalments and dates, agreed in writing, recovers more than an inflexible demand for full payment. Set clear deadlines for each instalment and enforce them. Placing the account on credit hold while a payment plan is in place protects against further credit exposure.

All communication at this stage should be logged. If the situation escalates further, a clear record of contact attempts, commitments made, and deadlines set is essential.

Step 7: Final Demand and External Collection (91+ Days Past Due)

Invoices past 90 days with no payment and no response to escalation efforts require a final formal demand before external action is considered. A final demand letter should state the amount outstanding, confirm the payment deadline, and make clear that failure to pay by that date will result in further action.

If the final demand is not met, the options are third-party collection agencies, legal proceedings, or a write-off. Third-party agencies work on a contingency basis, typically taking a percentage of any amount recovered. Legal proceedings are appropriate for high-value balances where the cost of litigation is proportionate to the potential recovery. Smaller balances may not justify the time and cost of legal action.

Step 8: Write-Offs and Bad Debt Management

A write-off is the accounting recognition that a receivable is no longer expected to be collected. It does not mean collection efforts must stop, but it removes the balance from AR and recognises the loss on the income statement. Most businesses apply a write-off policy based on invoice age: balances past 180 or more days with no contact or payment activity are strong candidates.

Document all collection activity before writing off any balance. Under GAAP, businesses are required to maintain an allowance for doubtful accounts, which is estimated using the aging schedule and applied as a provision before write-offs occur. Accurate documentation supports both the accounting treatment and any subsequent recovery efforts.

Best Practices for Optimising Your Collection Process

- Automate standard follow-up sequences: Manual reminders are inconsistent and inefficient at scale. Automation ensures every invoice receives appropriate follow-up at the right time without depending on individual team members to remember.

- Document your collection policy: A written policy with defined timelines, escalation paths, and authority levels removes guesswork from the process and ensures consistency across the team.

- Personalise communication: Customers who receive generic, templated communications are less likely to engage than those who receive professional, account-specific outreach. Reference the specific invoice, amount, and agreed payment terms in every contact.

- Offer flexible payment options: Multiple payment methods, including ACH, credit card, and online payment portals, reduce friction at the point of payment. Customers who can pay the way they prefer to pay are more likely to pay promptly.

- Incentivise early payment: Early payment discounts can accelerate cash collection from customers who have the liquidity to pay early. The cost of the discount should be weighed against your cost of capital and the collection efficiency gain.

- Review and adapt regularly: Collection processes that worked well at one transaction volume may break down at higher volumes. Review your process quarterly and adjust escalation timelines, communication templates, and automation rules based on what the data shows is working.

Legal Considerations in B2B Debt Collection

The Fair Debt Collection Practices Act (FDCPA) primarily governs consumer debt collection and applies limited protections in B2B contexts. However, state-specific commercial debt collection laws may apply, and best practice in B2B collections still requires professional, documented communication.

The statute of limitations for debt collection varies by state and contract type, typically ranging from three to six years. Invoices that pass the statute of limitations cannot be pursued through court action, though collection attempts can continue. Documentation of all collection activity is essential: it supports legal proceedings if required and demonstrates compliance with any applicable regulations.

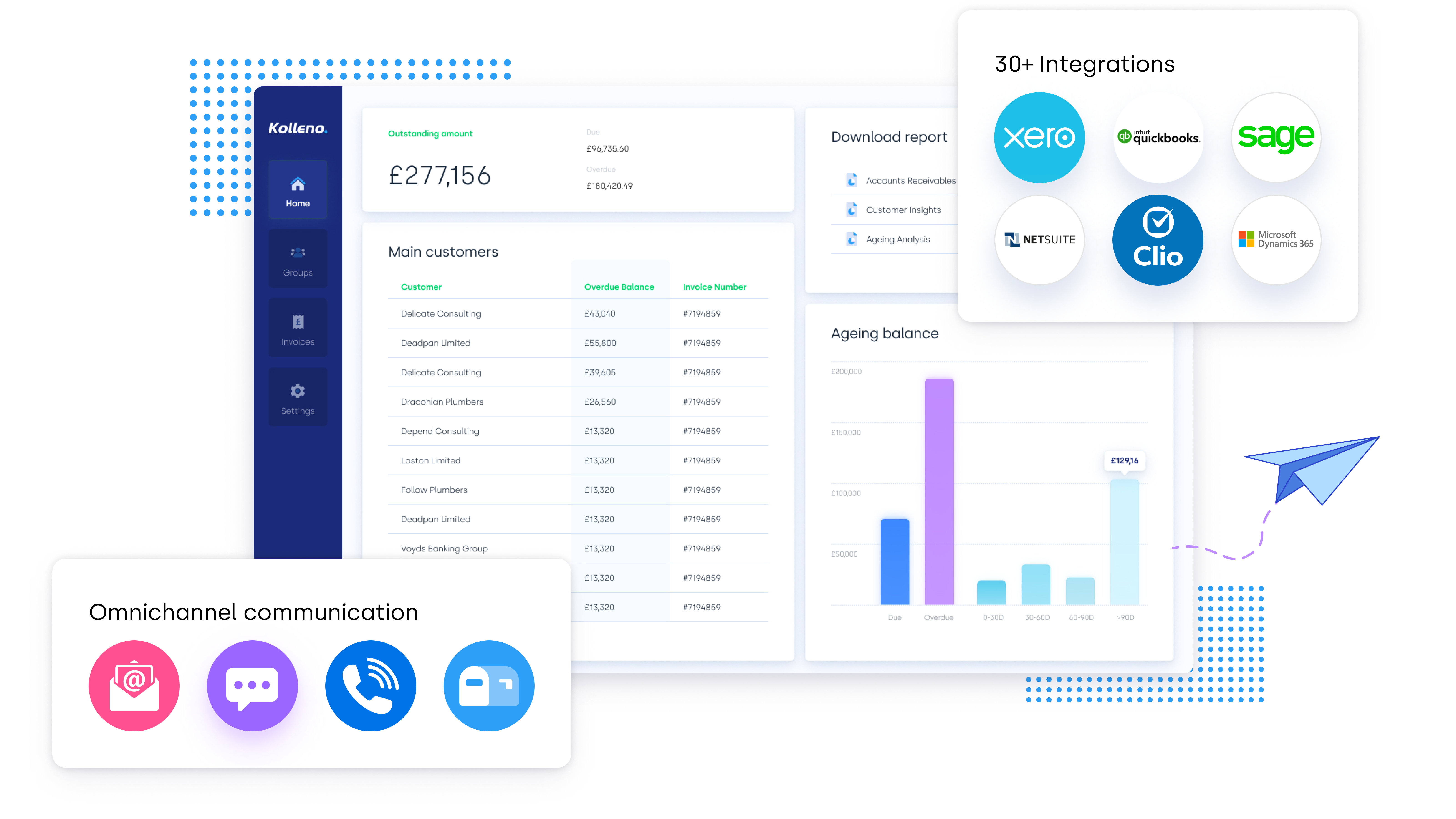

How Kolleno Supports the AR Collection Process

Kolleno’s O2C platform deploys AI Agents that handle collections outreach, follow-up sequencing, and escalation routing across your customer base. Finance teams configure the credit policy, collection rules, and escalation logic. Kolleno’s AI Agents execute them consistently, at scale, without manual intervention at each step.

The platform integrates with NetSuite, Microsoft Dynamics 365, Salesforce, HubSpot, Xero, QuickBooks, and other major systems. AR data stays current, and collection activity is logged automatically. Finance teams get visibility into every account’s collection status without compiling it manually and can focus their expertise on the accounts and decisions that genuinely require human judgment.

KPIs for Measuring Accounts Receivable Collections Effectiveness

Days Sales Outstanding (DSO)

DSO measures the average number of days it takes to collect payment. Declining DSO indicates that collections are improving. Rising DSO signals a problem that needs investigation: whether in credit policy, collection process, or customer payment behaviour.

Collection Effectiveness Index (CEI)

CEI measures how effectively your team is collecting receivables within a given period. It accounts for the ending AR balance, beginning AR balance, and credit sales, providing a more nuanced measure of collection performance than DSO alone.

Bad Debt Percentage

Bad debt as a percentage of total credit sales indicates how much of your revenue is ultimately unrecoverable. A rising ratio points to issues with credit policy, collections execution, or the risk profile of your customer base.

Average Days Delinquent (ADD)

ADD measures the average number of days invoices are overdue beyond their due date. Where DSO reflects the entire collection cycle, ADD focuses specifically on the delinquent portion, making it a more targeted indicator of collection effectiveness on overdue balances.

FAQs About the Accounts Receivable Process

What is the accounts receivable collection process?

The accounts receivable collection process is the sequence of steps a business takes to collect payment from customers for goods or services already delivered. It begins with credit assessment before a sale and progresses through invoicing, payment monitoring, reminders, escalating follow-up sequences, and, where necessary, external collection or legal action. The goal is to collect payment in full as efficiently and professionally as possible.

How do you improve accounts receivable collections?

Improvements typically come from three areas: process consistency, automation, and credit discipline. A documented collection policy with defined timelines and escalation paths produces more consistent results than an ad hoc approach. Automating standard follow-up sequences ensures every invoice is actioned on time. Tightening credit policy to reduce exposure to high-risk customers prevents overdue balances from accumulating in the first place.

What is the dunning process in accounts receivable?

Dunning is the systematic process of contacting customers to request payment of overdue invoices. A dunning sequence typically begins with a polite reminder shortly after the due date and escalates progressively in tone and channel as the invoice ages. Automated dunning ensures that every overdue invoice receives consistent follow-up without requiring manual action at each step in the sequence.

When should you use a collections agency?

A third-party collections agency is typically appropriate for invoices that are 90 or more days past due, where internal collection efforts have been exhausted, and direct contact with the customer has failed. Agencies work on contingency, taking a percentage of any recovered amount. Legal proceedings are a separate escalation path for high-value balances where the cost of litigation is proportionate to the potential recovery.

Final Thoughts

The accounts receivable collection process is most effective when it’s consistent, documented, and supported by technology that handles routine execution at scale. Finance teams that combine a clear credit policy with a systematic collection sequence and real-time AR visibility consistently outperform those managing collections reactively.

If you want to see how Kolleno’s AI Agents manage collections execution across your customer base, book a demo of Kolleno.

- Why an Effective AR Collection Process Matters

- Common Challenges in AR Collections

- The Step-by-Step AR Collection Process

- Step 1: Credit Management and Customer Onboarding

- Step 2: Accurate and Timely Invoicing

- Step 3: AR Monitoring and Aging Reporting

- Step 4: Pre-Due-Date and Due-Date Reminders

- Step 5: First Follow-Up for Overdue Invoices (1-30 Days Past Due)

- Step 6: Escalation and Negotiation (31-90 Days Past Due)

- Step 7: Final Demand and External Collection (91+ Days Past Due)

- Step 8: Write-Offs and Bad Debt Management

- Best Practices for Optimising Your Collection Process

- Legal Considerations in B2B Debt Collection

- How Kolleno Supports the AR Collection Process

- KPIs for Measuring Accounts Receivable Collections Effectiveness

- FAQs About the Accounts Receivable Process

- Final Thoughts