Accounts receivable collection is the process of recovering outstanding payments from customers who have purchased on credit. It is one of the most consequential functions in finance: done well, it keeps cash flowing and reduces bad debt. Done poorly, it creates a compounding problem that affects liquidity, financial reporting, and customer relationships alike.

This guide covers the full picture: what AR collections involve, how to run them effectively, how to measure performance, and how to make the right decisions when accounts go past due.

What Are Accounts Receivable Collections?

Accounts receivable collections is the activity of recovering payments owed to a business for goods or services delivered on credit. It is the collections phase of the credit-to-cash process: the point where an invoice has been issued, the due date has passed, and the business is actively working to receive what it is owed.

AR collections covers everything from sending the first payment reminder to, in extreme cases, writing off an account as bad debt. Between those two points lies a structured process of follow-up, escalation, dispute resolution, and negotiation. The goal is to collect as much as possible, as quickly as possible, while keeping the customer relationship intact wherever that is appropriate.

Why Effective AR Collections Is Critical for Business Health

Cash flow is the oxygen of any business. AR that sits uncollected does not just look bad on a report. It ties up capital that could be invested, it forces businesses to draw on credit lines to cover operating costs, and it increases the risk of write-offs that hit the income statement directly.

Effective AR collections reduce Days Sales Outstanding (DSO), the primary measure of how quickly a business converts sales into cash. A lower DSO means more predictable cash flow, less dependence on external financing, and a healthier balance sheet.

Revenue recognition is also at stake. Accounts that go uncollected are eventually written off, reversing revenue that was previously reported. Strong collections protect the integrity of financial reporting as well as the cash position.

Customer relationships matter here, too. A professional, consistent, and empathetic collections process can resolve late payments without damaging the commercial relationship. Many late payments result from administrative issues on the customer’s side, not from an intent to default.

The Accounts Receivable Collection Process: A Step-by-Step Guide

Effective accounts receivable collections follow a structured process, from preventing late payments to recovering long-overdue debts. While every organization may have its own procedures, most collections workflows follow the same three stages: prevention, active collection, and escalation.

1. Pre-Collection: Preventing Late Payments

The strongest collections strategies begin before an invoice becomes overdue. Send accurate invoices promptly, establish clear payment terms, and communicate credit policies upfront to eliminate confusion.

A few days before the due date, send a friendly reminder to encourage timely payment and reduce the likelihood of delinquency.

2. Active Debt Collection: Managing Overdue Accounts

When an invoice becomes overdue, collection efforts begin. Use AR aging reports to prioritize accounts based on how long balances have remained unpaid and focus resources on higher-risk invoices.

Follow a structured dunning process that escalates from automated reminders to phone calls and formal notices. For larger accounts, personalized outreach can help uncover disputes, cash flow challenges, or administrative issues that may be delaying payment.

3. Dispute Resolution and Escalation

Payment disputes should be investigated and resolved as quickly as possible, as unresolved issues are a common cause of delayed collections. Establish a clear process for logging, reviewing, and responding to disputes.

If payment remains outstanding despite standard follow-up, escalate according to your collections policy. This may include management involvement, demand letters, credit holds, or other formal actions.

4. Last Resort Recovery Measures

When internal collection efforts fail, businesses may refer accounts to a collection agency or pursue legal action where appropriate. The best option depends on the debt value, likelihood of recovery, and applicable regulations.

If recovery is no longer considered viable, the account may be written off as bad debt in accordance with company policy and accounting requirements.

Strategies and Best Practices to Improve AR Collections

Improving accounts receivable collections requires more than persistent follow-up. The most successful organizations combine efficient payment processes, proactive customer communication, and strong internal controls to reduce overdue balances and accelerate cash flow.

Optimize Invoicing and Payment Systems

Make Payments Easy

The easier it is for customers to pay, the faster invoices are typically collected. Offer multiple payment methods, including ACH, credit and debit cards, and online payment portals. Where appropriate, early payment incentives such as 2/10 Net 30 can encourage faster settlement.

For recurring revenue models, automated invoicing and payment schedules help reduce administrative delays and improve consistency.

Improve Invoice Accuracy and Clarity

Clear, accurate invoices eliminate common payment obstacles. Every invoice should include itemized charges, payment instructions, due dates, and relevant purchase order information.

Standardized invoice templates can reduce errors, improve consistency, and make it easier for customers to process payments promptly.

Strengthen Customer Communication

Follow Up Early and Consistently

Collection efforts should begin as soon as an invoice becomes overdue. Prompt, professional outreach demonstrates that accounts are actively monitored and often prevents minor delays from becoming larger collection issues.

A structured reminder schedule helps ensure no account falls through the cracks.

Use Multiple Communication Channels

Different customers prefer different communication methods. Combining email reminders, phone calls, SMS messages, and customer portal notifications often generates better response rates than relying on a single channel.

A multi-channel approach also increases the likelihood that payment requests reach the appropriate decision-maker.

Personalize Collection Efforts

Not all late payments have the same cause. Some customers may be experiencing cash flow constraints, while others may be dealing with administrative issues or invoice disputes.

Understanding the reason behind a delayed payment allows collection teams to tailor their approach and resolve issues more effectively.

Invest in Collections Training

Successful collections require strong interpersonal skills as well as process knowledge. Training should focus on communication, negotiation, conflict resolution, and identifying the difference between customers who cannot pay and those who are simply unwilling to prioritize payment.

Well-trained AR teams often achieve better results than organizations that rely solely on stricter collection policies.

Strengthen Internal Processes and Risk Management

Align Teams Around Collection Goals

Accounts receivable performance improves when sales, finance, and customer service teams work together. Sales teams may have valuable customer relationships that help resolve payment issues, while customer service teams often have visibility into disputes or fulfillment concerns.

Cross-functional collaboration can accelerate issue resolution and reduce payment delays.

Reduce Customer Concentration Risk

Businesses that rely heavily on a small number of customers face greater exposure when a major account pays late or defaults. Diversifying the customer base helps reduce this risk and creates a more stable cash flow position.

Review Credit Risk Regularly

Customer financial health and payment behavior can change over time. Regular credit reviews help ensure that credit limits and payment terms remain aligned with current risk levels.

For key accounts, annual or semi-annual reviews can help identify emerging risks before they lead to collection problems.

Key Performance Indicators (KPIs) for AR Collections

Tracking the right KPIs helps finance teams measure collection performance, identify emerging risks, and improve cash flow management. While many metrics are available, a handful provide the clearest picture of accounts receivable health.

Days Sales Outstanding (DSO)

Days Sales Outstanding (DSO) measures the average number of days it takes to collect payment after a sale is made. It is one of the most widely used accounts receivable metrics because it provides a quick snapshot of collection efficiency.

Formula:

DSO = (Accounts Receivable ÷ Net Credit Sales) × Number of Days

A rising DSO may indicate slower customer payments, inefficient collection processes, or increasing credit risk.

Collection Effectiveness Index (CEI)

The Collection Effectiveness Index (CEI) measures how effectively your team collects available receivables during a specific period. Unlike DSO, it accounts for new invoices generated during the reporting period, making it a more precise measure of collection performance.

A higher CEI generally indicates a more effective collections process.

Accounts Receivable Turnover Ratio

The Accounts Receivable Turnover Ratio shows how many times receivables are collected and replaced over a given period.

Formula:

ART = Net Credit Sales ÷ Average Accounts Receivable

A higher turnover ratio typically reflects faster collections and stronger cash flow management.

Aging Report Performance

An AR aging report categorizes outstanding invoices based on how long they have been overdue. Monitoring the distribution across aging buckets helps identify collection trends and prioritize follow-up efforts.

A growing percentage of balances in the 61–90 day or 90+ day categories may signal elevated collection risk.

Bad Debt Ratio

The Bad Debt Ratio measures the percentage of receivables that ultimately become uncollectible and must be written off.

An increasingly bad debt ratio may suggest weaknesses in credit approval processes, customer screening, or collection escalation procedures.

Challenges in AR Collections and How to Overcome Them

Effective accounts receivable (AR) collections require more than consistent follow-up. Teams often face obstacles that slow recovery efforts, increase administrative workloads, and create compliance risks. Understanding these common challenges and implementing the right processes and technology can help improve collection outcomes while maintaining positive customer relationships.

Lack of Account Prioritization

Lack of account prioritization is one of the most common collections challenges. Without a data-driven approach to prioritizing follow-up, teams often focus on recent invoices rather than the highest-risk aged debt. Use your aging report and payment history to rank accounts by urgency.

Manual Outreach and Follow-Up Management

Manual outreach at scale is time-consuming and error-prone. Teams managing hundreds of accounts through email and spreadsheets may miss follow-ups, send duplicate messages, and lack a consolidated view of where each account stands. Automation helps address these challenges by streamlining communications, scheduling follow-ups, and centralizing account information.

Legal and Regulatory Compliance

Legal compliance is a frequently overlooked area of AR collections. In the US, the FDCPA applies to third-party collectors. For in-house collections, state-level regulations may apply depending on the nature of the debt and the customer. For international collections, GDPR and equivalent privacy laws affect how customer data can be used. Because requirements vary by jurisdiction and circumstances, organizations should seek qualified legal advice to ensure their collections processes remain compliant.

In-House vs. Outsourced Collections: A Practical Comparison

In-house collections give you direct control over the process, customer communication, and brand representation. You retain full visibility into account status, and your team can draw on the wider customer relationship when navigating a difficult conversation. The trade-off is cost: internal AR staff, systems, and management overhead add up, and your team’s capacity to pursue every overdue account is limited.

Outsourced collections, through a third-party agency, add specialist capacity and remove some of the operational burden. Agencies typically work on contingency and have recovery-focused processes and systems.

The trade-off is reduced control over how your customers are contacted, and the agency takes a percentage of what it recovers. For very old or high-volume low-value debt, outsourcing often makes economic sense. For strategically important customer relationships, keeping collections in-house is usually the right call.

The Role of AR Collection Software and Automation

AR automation platforms reduce the manual workload involved in collections while improving consistency and coverage. Automated dunning sequences send reminders on a fixed schedule without human intervention. Payment portals allow customers to view and pay invoices without waiting for a finance team member to process a payment manually. Real-time aging dashboards give collections teams immediate visibility into which accounts need attention.

AI-driven prioritization takes this further. Rather than treating all overdue accounts equally, AI can rank accounts by the combination of amount outstanding, days overdue, payment history, and other signals, so collections teams focus their human effort where it has the most impact.

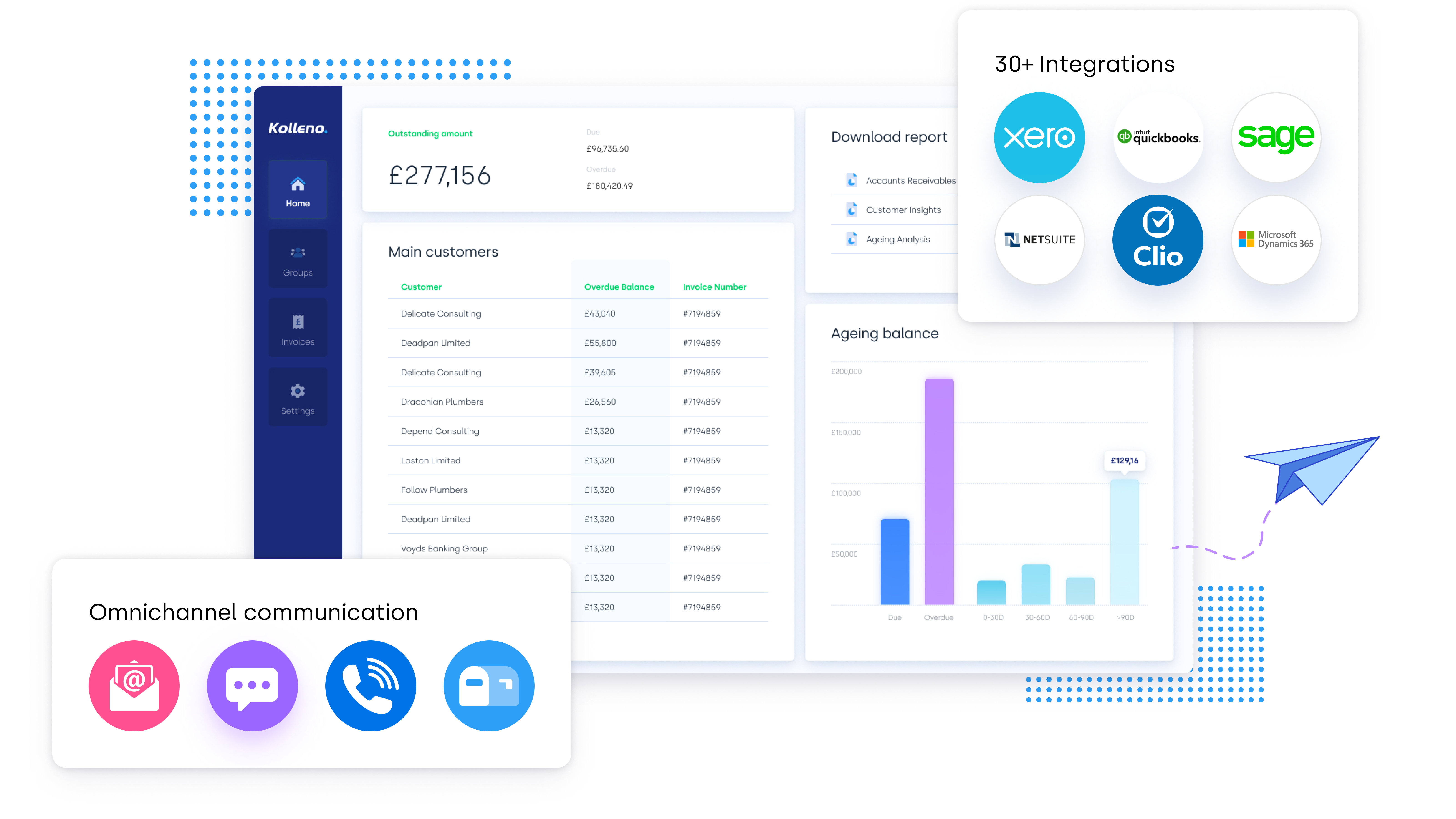

Integration with ERP systems including NetSuite, QuickBooks, Xero, Sage Intacct, Microsoft Dynamics, Oracle Fusion, and SAP is essential. An AR platform that operates in isolation from the rest of the finance stack creates reconciliation problems and duplicated data entry.

How Kolleno Supports AR Collections

Kolleno’s O2C platform deploys AI Agents that function as an operational extension of the finance team. These digital workers handle collections outreach, cash application, dispute routing, and reporting autonomously, executing according to the policies your team defines. Finance professionals orchestrate strategy and manage exceptions. The AI Agents handle execution.

If you want to see what a collections process built on AI Execution looks like in practice, book a demo of Kolleno.

Frequently Asked Questions

How do you record the collection of accounts receivable?

When a customer payment is received, debit Cash and credit Accounts Receivable. This removes the outstanding balance from AR and records the incoming cash.

If a payment was previously written off as bad debt and the customer later pays, first reverse the write-off: debit accounts receivable and credit allowance for doubtful accounts. Then record the payment normally: debit Cash, credit Accounts Receivable.

What KPIs should I track for AR collections?

The most important AR collections KPIs are Days Sales Outstanding (DSO), which measures how long it takes to collect payment after a sale; the Collection Effectiveness Index (CEI), which measures the percentage of collectable AR that was actually collected; the Accounts Receivable Turnover ratio; and the Bad Debt Ratio. Reviewing the aging report distribution weekly provides an operational view of where collections attention is most needed.

How do I collect payments without damaging customer relationships?

Start early and stay professional. Send reminders before the due date, not just after. When follow-up is needed, lead with questions rather than accusations: confirming the invoice was received and understanding if there are any issues signals good faith.

Offer payment plans where appropriate. Reserve escalating language and formal notices for accounts that have not responded to earlier, less formal outreach.

What happens to uncollectible accounts receivable?

When an account is confirmed uncollectible, the balance is written off. Under the allowance method, the write-off is applied against the existing Allowance for Doubtful Accounts balance: debit Allowance for Doubtful Accounts, credit Accounts Receivable.

Under the direct write-off method, it is: debit Bad Debt Expense, credit Accounts Receivable. Writing off an account does not legally extinguish the debt. Businesses can still pursue collection through an agency or legal action after a write-off.

- What Are Accounts Receivable Collections?

- Why Effective AR Collections Is Critical for Business Health

- Strategies and Best Practices to Improve AR Collections

- Key Performance Indicators (KPIs) for AR Collections

- Challenges in AR Collections and How to Overcome Them

- In-House vs. Outsourced Collections: A Practical Comparison

- The Role of AR Collection Software and Automation

- How Kolleno Supports AR Collections

- Frequently Asked Questions