For small businesses, extending credit can feel like a double-edged sword. On one side, it builds trust, fuels sales, and supports business growth. On the other, it can drain cash flow and leave owners chasing late payments or writing off unpaid debts. Too much credit creates risk. Too little, and you risk losing customers to competitors willing to offer credit more freely.

That’s why every SME needs a clear, structured credit policy. It’s the blueprint for how you grant credit, set credit limits, and manage customer relationships. The right credit policy protects against poor credit management and keeps business finances stable, ensuring timely payments.

In this article, we’ll explain how SMEs can build and implement a robust credit policy for their specific needs.

What Is a Credit Policy and Why Is It Essential?

A credit policy is a set of rules that defines how your business decides to extend credit to customers. It covers everything from credit applications and approval processes to the credit terms you offer and the steps you’ll take if customer payments fall behind. For business owners, it’s both a shield and a guide—helping them make informed decisions while keeping the company’s cash flow protected.

Without a clear policy, small businesses often drift into loose credit practices: offering flexible credit to win sales, but without limits or checks. That approach might boost revenue in the short term, but it quickly leads to slow payments, late payments, and even non payment. In contrast, a well-defined business credit policy balances risk and reward. It lays out how much credit to offer, to whom, and under what credit conditions, giving everyone—from the sales team to the credit manager—a consistent framework to follow.

The real strength of a formal credit policy lies in its role as a risk management tool. By standardising the credit process, it helps prevent poor credit management and keeps business credit exposure under control. And because it forces discipline in setting credit limits and monitoring customer creditworthiness, it ensures your business is less exposed to shocks, whether they come from individual customers or broader market volatility.

Key Elements of a Robust Credit Policy

A strong credit policy gives business owners the structure they need to balance growth with protection. These are the building blocks every SME should include.

Credit Applications

The process starts with a formal credit application. This collects essential information on new customers and existing customers, from company details to trade references. It’s your chance to set expectations and gather the data you’ll use to assess credit risk.

Assessing Creditworthiness

No two customers are the same, which is why every application should be backed by a proper risk assessment. That might include pulling a credit report, checking credit scores, reviewing payment history, and analysing financial statements. Together, these steps help you judge customer creditworthiness and decide whether to offer credit—and if so, on what terms.

Setting Credit Limits

One of the most important parts of any business credit policy is deciding how much credit to extend. Setting appropriate credit limits protects your company’s cash flow and avoids overexposure. Limits should reflect not just a customer’s profile, but also your own business finances, profit margins, and appetite for financial risk.

Credit Terms

A robust policy also defines your credit terms. These outline payment terms (for example, net 30 days), penalties for late payments, and incentives such as early payment discounts. Consistent, transparent terms keep customer relationships clear and reduce the chance of disputes.

Documentation and Communication

Even the best policy fails if it’s not communicated. Make sure your credit conditions are written into contracts, agreements, and even your invoice templates. This provides clarity for customers and ensures your team can enforce policies consistently.

Putting Your Credit Policy Into Practice

A well-written credit policy only works if it’s applied consistently. For small businesses, that means turning principles into daily routines—checking new applications carefully, monitoring customer payments, and acting quickly when problems arise. Here’s how to make your policy work in practice.

1. Screen Every Application Thoroughly

Never skip the basics. Every credit application should include a credit check, a review of credit reports, and where possible, analysis of financial statements. This ensures you only grant credit to customers who can meet their financial obligations.

2. Set and Enforce Credit Limits

Once you’ve decided to offer credit, determine how much credit is appropriate. Setting credit limits based on customer creditworthiness and your own business finances protects your company’s cash flow. Enforce these limits strictly to avoid overexposure.

3. Define and Monitor Credit Terms

Be clear about credit terms from day one—whether it’s net 30 days, staged payments, or incentives like early payment discounts. Track compliance closely, using tools like payment reminders or accounting software to reduce late payments and maintain timely payments.

4. Monitor Customer Payments and Behavior

Don’t stop at onboarding. Monitor payment history and patterns of payment behavior with both new customers and existing customers. Early detection of slow payments or signs of non payment allows you to intervene before debts spiral.

5. Have a Debt Collection Plan

Even with strong policies, some debts will slip. Include clear debt collection strategies in your framework—from friendly reminders to structured debt collection processes. Escalate consistently, so customers know you take credit control seriously.

6. Review and Adjust Regularly

No policy should be static. Review your business credit policy at least annually, and more often if you’re facing market volatility or industry-specific challenges. Reassess credit limits, refresh your approval processes, and adapt terms to protect profit margins.

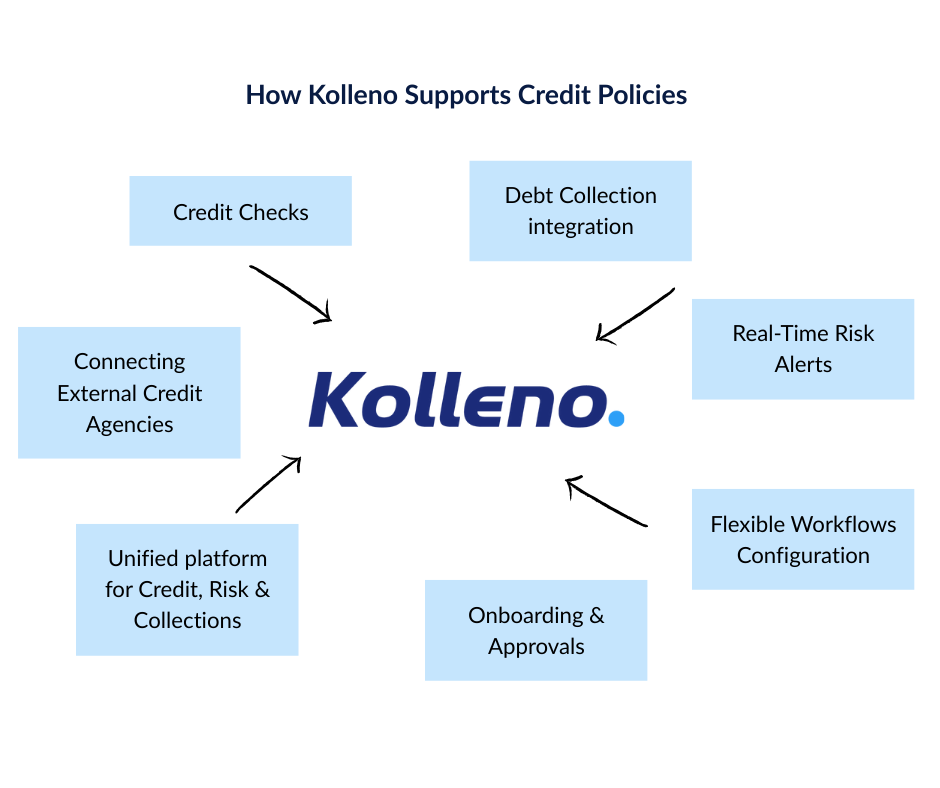

How Kolleno Supports SME Credit Policies

For small businesses, the challenge isn’t just writing a credit policy—it’s applying it consistently across customers, teams, and markets. That’s where Kolleno comes in. The platform automates the hard parts of credit management, giving SMEs the tools to enforce their policies without slowing down sales or stretching finance teams.

Kolleno automates new client credit checks and integrates with external credit agencies to provide up-to-date reports, ensuring every decision to extend credit is based on accurate data. Once a customer is onboarded, Kolleno continuously monitors risk exposure and sends real-time credit alerts if a profile changes, so business owners can adjust credit limits or credit terms before problems escalate.

The platform also unifies credit, risk, and collections data into a single system. That means credit managers can design workflows that reflect their own business credit policy, from setting approval processes to defining clear steps for addressing at-risk accounts. And when debt collection becomes necessary, Kolleno connects SMEs with local and international agencies to recover outstanding balances—helping you manage cash flow without damaging customer relationships.

In short, Kolleno turns a written credit policy into a working system. By embedding automation into daily operations, it helps SMEs protect against late payments, prevent unpaid debts, and maintain the discipline needed for long-term financial stability.

Final Thoughts

A robust credit policy is one of the most valuable tools an SME can have. It keeps cash flow predictable, protects against late payments, and ensures that every decision to extend credit supports rather than undermines business growth. But even the best-written policy can fail if it isn’t applied consistently.

That’s where automation makes the difference. Platforms like Kolleno embed policies into daily operations—running real-time credit checks, monitoring credit limits, and streamlining debt collection when needed. The result is an approach to credit management that’s not just compliant, but proactive, disciplined, and scalable.

Ready to strengthen your SME’s credit policy? Book a demo with Kolleno today and see how automation helps you turn policy into practice.